Should Homemakers Have Life Insurance? Explained

Table of Contents

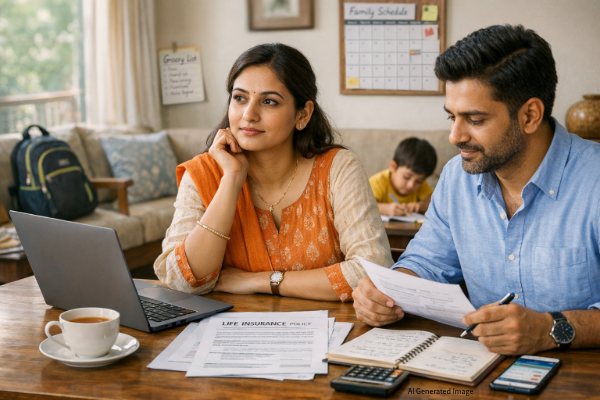

Discover Should homemakers have life insurance? A complete guide for Indian families. Learn why life insurance for homemakers matters, how much coverage you need and how to buy a policy in India.

When most families sit down to plan their finances, life insurance conversations almost always revolve around the earning member. The logic feels solid: protect the salary, protect the family. But this approach misses something important that financial planners often flag.

A homemaker does not earn a salary. But they perform work every single day that keeps the household running smoothly. Cooking, childcare, managing school schedules, handling household budgets, and caring for elderly parents these are not small contributions. If you had to hire professionals to replace each of these roles, your monthly expenses would climb sharply.

So the real question is not whether a homemaker earns money. The right question is: what would it actually cost your family if the homemaker were no longer there?

That answer often surprises people. And it is the reason life insurance for homemakers deserves a place in every family’s financial plan.

The Hidden Financial Value of Homemakers

Picture a typical day for a homemaker. They are up early, preparing meals, getting children ready for school, managing grocery lists, tracking household bills, and coordinating doctor appointments. By evening, they have done the combined work of a cook, a nanny, a housekeeper, and a household administrator.

None of this work appears in a salary statement. But it all has a market value.

If a family in a city like Mumbai, Bengaluru, or Delhi had to hire paid professionals to replace these services, the monthly cost could easily range from Rs 30,000 to Rs 60,000. That figure covers a full-time domestic helper, a cook, a childcare professional, and part-time elder care support.

On an annual basis, that works out to Rs 3.6 lakh to Rs 7.2 lakh in extra household expenditure. The economic contribution of a homemaker is substantial, even if it never shows up on a payslip.

This is why many financial planners today recommend including life insurance for homemakers as a core part of family protection planning not as an afterthought.

What Happens Financially If a Homemaker Is Not Around?

This is a difficult topic to discuss, but responsible financial planning means asking hard questions before a crisis makes the decision for you.

If a homemaker passes away unexpectedly, the financial disruption can hit from multiple directions at the same time. Here is what most families face:

- The cost of hiring a full-time nanny or childcare professional rises immediately.

- Daily cooking, cleaning, and household management now come at a paid cost.

- The working spouse may need to reduce work hours or take extended leave to manage the household.

- Children’s routines are disrupted, often leading to added spending on tutoring, activity support, or counselling.

- Elder care needs that the homemaker was managing may require paid professional support.

At a time when the family is already grieving, they also face a sudden spike in monthly expenses. That combined financial and emotional pressure is exactly what life insurance for homemakers is designed to address.

How Life Insurance Helps Protect the Family

Life insurance for a homemaker works differently from a standard income protection plan. There is no salary to replace. The purpose here is to fund the cost of services the homemaker provided, so the family does not face a financial crisis on top of a personal tragedy.

A life insurance payout in this situation can help the family in several practical ways:

- Cover the cost of hiring childcare and domestic support for several years.

- Manage the sharp increase in monthly household expenses.

- Keep the children’s education plans on track without financial compromise.

- Give the surviving spouse time to grieve, reorganize, and adapt without immediate money pressure.

- Provide financial stability during one of the most emotionally difficult periods in a family’s life.

- Offer a tax benefit: premiums paid on a term life insurance plan are eligible for deduction under Section 80C of the Income Tax Act, 1961, up to Rs 1.5 lakh per year.

Think of life insurance as a financial cushion during the transition. It does not undo the loss, but it removes the financial strain that would otherwise compound an already painful situation.

Can Homemakers Buy Life Insurance in India?

Yes, homemakers can purchase life insurance in India. The option is available, though the process works a little differently compared to a salaried applicant.

Since a homemaker has no declared personal income, insurance companies assess the policy based on several alternative factors:

- The income and existing life insurance coverage of the earning spouse.

- The overall financial profile and lifestyle of the household.

- The financial justification provided for the sum assured being requested.

- The number of dependents and the household’s monthly expenses.

Many insurers in India also apply a cap on the coverage a homemaker can take out, typically limiting it to 25% to 50% of the earning spouse’s existing sum assured. For example, if the spouse holds a Rs 1 crore policy, the homemaker may be eligible for Rs 25 lakh to Rs 50 lakh in coverage, though some insurers now extend this up to Rs 1 crore for higher-income households. Homemaker eligibility is determined by each insurer’s own Board Approved Underwriting Policy, so rules vary across companies. Comparing options before committing is always a good idea.

What Type of Life Insurance Is Suitable?

For most families, term insurance is the most practical and cost-effective choice for a homemaker.

Term insurance is pure protection. You pay a relatively low premium in exchange for a high sum assured. If the insured person passes away during the policy term, the nominee receives the full payout. There are no investment elements, no maturity benefits, and no complexity.

This straightforward structure makes term insurance especially useful when the goal is financial protection for the family, not building a corpus or earning returns. A Rs 40 lakh term insurance policy for a homemaker typically costs a fraction of what an endowment or ULIP plan would charge for the same coverage.

Other plan types like endowment policies or unit-linked insurance plans (ULIPs) are available too, but they come with significantly higher premiums for the same level of life cover. For families where protecting the household is the primary goal, term insurance gives the most coverage per rupee spent.

How Much Life Insurance Should a Homemaker Have?

The right coverage amount depends on what it would realistically cost to replace the homemaker’s contribution to the household.

Many financial planners suggest starting with coverage between Rs 20 lakh and Rs 50 lakh as a baseline. For metro-city families with young children and no support network, the need could be higher. Several insurers today offer homemaker policies going up to Rs 1 crore, subject to the spouse’s income and overall financial profile. The ideal number depends on your family’s specific circumstances, including:

- Number and age of children at home.

- Monthly cost of domestic help and childcare in your city.

- Total household expenses the homemaker currently manages.

- Availability of extended family support.

- How long financial support would be needed before the household stabilizes.

A family with two young children in a metro city and no nearby relatives will need significantly more coverage than a household with adult children and strong community support.

A Simple Way to Estimate Coverage

You do not need a financial advisor to get a rough coverage estimate. A simple calculation works well for most families.

Step 1: List all the household tasks the homemaker currently handles cooking, childcare, cleaning, elder care, household management.

Step 2: Estimate the monthly cost of hiring paid professionals to replace each of those tasks in your city.

Step 3: Multiply the annual cost by the number of years you want the coverage to last, typically 10 to 15 years.

Practical example: Suppose the total monthly replacement cost in your city is Rs 30,000. That is Rs 3.6 lakh per year. Multiplied by 10 years, you arrive at an estimated coverage need of around Rs 36 lakh.

This method is not a precise formula, but it gives you a grounded, practical number to work with when exploring policies.

When Life Insurance for Homemakers Becomes Important

There are certain family situations where taking life insurance for a homemaker becomes especially critical.

Young children at home is the clearest trigger. If the homemaker is the primary caregiver for children below 10 to 12 years of age, the cost of replacing that care is both high and immediate.

It becomes equally important when the working spouse holds a demanding job that leaves little flexibility for household management. If the entire domestic operation depends on one person, the financial gap from losing them is enormous.

Families who live away from parents or extended relatives also face a higher financial risk. Without an informal support network, every gap needs to be filled with paid help.

In all these situations, life insurance for homemakers is not a luxury. It is a genuinely practical part of family financial planning.

Situations Where It May Be Less Necessary

Life insurance for a homemaker is not essential in every household. There are situations where the need is naturally lower.

If the children are adults and financially independent, the financial impact of losing a homemaker on household expenses is significantly reduced. Similarly, if grandparents or other family members are actively involved in childcare and daily household management, the reliance on the homemaker is smaller.

If the earning spouse already carries a very high sum assured that can comfortably absorb additional household expenses for several years, a separate policy for the homemaker may carry less urgency.

That said, financial decisions should always reflect the full picture of your household. What seems unnecessary today can look very different three or five years from now.

Key Takeaway

A homemaker may not bring home a salary, but their contribution to the family carries real, measurable financial value. The services they provide every day, from childcare to household management, would cost the family a substantial amount to replace.

If their absence would create financial strain, which it would in most households with young children, then life insurance for homemakers is not just a thoughtful gesture. It is a smart and responsible financial decision.

Even a modest term insurance policy provides the family with financial breathing room during one of the hardest periods they will face. It keeps education plans intact, covers household expenses, and allows the surviving spouse to focus on their family rather than a financial crisis.

Complete family financial protection means protecting every person who contributes to the household. Not just the one with the salary slip.