Evaluate Financial Risk Without Fear (The Ultimate Guide)

Table of Contents

Learn how to evaluate financial risk without fear. Practical tips to invest confidently, manage uncertainty and make smarter money decisions.

Picture two neighbours in the same housing society. One refuses to touch the stock market because “it’s too risky.” The other invests every month, rain or shine, without losing sleep over red days in the market. Same income bracket, same city, completely different relationship with risk.

The difference isn’t luck. It’s understanding.

Most money mistakes don’t come from taking risks. They come from taking risks people don’t understand, or running away from every opportunity because fear has taken the wheel. When markets fall, some investors panic and sell at the worst possible time. When markets rally, others jump into investments they barely understand because they’re afraid of missing out.

The real issue was never risk itself. It’s making decisions without evaluating that risk properly. Once you learn to evaluate financial risk without fear clouding your judgment, you stop reacting and start deciding.

What Financial Risk Actually Means

Ask ten people what financial risk means and most will say “losing money.” That’s only half the picture. Financial risk is really the gap between what you expect from a decision and what actually happens. Sometimes that gap works in your favour. Sometimes it doesn’t.

Every money decision carries some uncertainty, whether you’re buying mutual funds, purchasing property, switching jobs, lending money to a relative, or simply parking your savings in a bank account.

Here’s the part most people miss. Avoiding risk altogether creates its own set of problems. Inflation quietly eats into your purchasing power every year. Keeping all your money in a savings account feels safe but limits long term wealth creation. Skipping investments entirely makes goals like retirement or your child’s education harder to fund.

The goal was never to eliminate risk completely. It’s to understand it, measure it and manage it on your terms.

Why Fear Hijacks Good Financial Decisions

Fear is hardwired into us. It once protected our ancestors from real danger, but in personal finance, that same instinct often works against us. Fear pushes people to sell investments the moment markets dip, delay investing for years waiting for the “right time,” avoid learning about money altogether, and react to every piece of negative financial news.

Notice the pattern. Fear obsesses over what could go wrong while completely ignoring what could go right. Smart investors don’t switch fear off. They simply stop letting it make decisions for them.

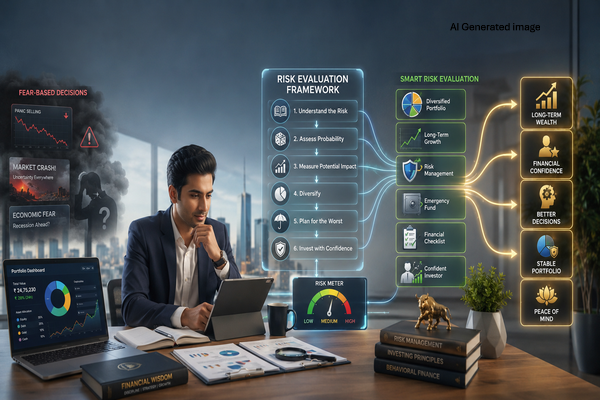

A Practical Framework to Evaluate Risk

Step 1: Get Clear on Your Goal

Before evaluating any investment, ask what you’re actually trying to achieve. Retirement, a house down payment, your child’s education or simply building an emergency cushion all call for different risk levels. Without a clear goal, you can’t judge whether a risk is even worth taking.

Step 2: List What Could Go Wrong

If you’re investing in equity, think through market corrections, company specific issues and economic slowdowns. If you’re buying real estate, factor in falling property prices, vacant periods and unexpected repair costs. Writing these down makes risks feel manageable instead of vague and scary.

Step 3: Estimate the Probability

Has this kind of risk played out before? How often? Separating what’s merely possible from what’s actually probable is one of the most underrated financial skills. Just because a crash can happen doesn’t mean one is likely next month.

Step 4: Weigh the Real Impact

If the risk materialises, how much would you actually lose? Would your lifestyle take a hit? How long would recovery take? Two investments can carry similar odds of loss but very different consequences, so impact deserves as much attention as probability.

Step 5: Compare Risk With Reward

Stop asking “can I make money here?” Start asking “is this reward worth the risk I’m taking?” Higher potential returns usually come with higher volatility, though the relationship isn’t fixed across every asset class. This single mindset shift improves decision quality immediately.

Step 6: Know Your Own Risk Appetite

Risk tolerance is personal. Two people earning identical salaries can have wildly different comfort levels with market swings, shaped by age, job stability, family responsibilities and past investment experience. There’s no universally right answer, only the strategy you can stick with through both bull and bear markets.

Step 7: Diversify Instead of Predicting

Nobody can consistently call market tops and bottoms. Spreading money across equity, debt, gold and real estate, depending on your goals, reduces the damage from any single bad bet. Diversification softens losses, but it cannot guarantee profits or eliminate risk entirely.

Step 8: Build Your Safety Net First

Taking calculated investment risk becomes far easier once your foundation is solid. A widely recommended starting point is keeping three to six months of essential expenses as an emergency fund, though the right number depends on your income stability and family situation. This cushion stops you from making panicked, emotional decisions during a crisis.

Step 9: Ignore the Headlines, Trust the Plan

Financial news thrives on alarm because alarm gets clicks. Before reacting to a scary headline, ask whether your long term goal has actually changed or whether you’re simply reacting emotionally. Long term investors who focus on fundamentals usually outperform those glued to daily market noise.

Step 10: Judge the Decision, Not Just the Outcome

Even a well researched decision can underperform in the short run, and a poorly thought out one can occasionally get lucky. Instead of judging yourself by results alone, ask if you researched properly, understood the risks and stayed aligned with your goals. A solid process compounds into better outcomes over time.

Mistakes That Quietly Sabotage Smart Investors

Watch out for investing simply because everyone around you is doing it, trusting “guaranteed return” schemes that promise high returns with zero risk, chasing last year’s best performing fund without checking if it suits your goals, ignoring inflation while sitting entirely in cash, and letting short term emotions override a long term plan.

Final Thoughts

Fear is natural, but it doesn’t have to steer your financial future. Every meaningful money decision carries some uncertainty. Instead of avoiding risk altogether, focus on understanding it, preparing for it and managing it deliberately.

Get clear on your goals, build an emergency fund, diversify sensibly and review your portfolio periodically instead of obsessing over it daily. Confidence in money decisions doesn’t come from eliminating risk. It comes from understanding exactly what you’re signing up for.

Sometimes the biggest financial risk isn’t taking a chance. It’s letting fear stop you from taking one at all.

FAQs

What does it mean to evaluate financial risk?

Evaluating financial risk means identifying possible risks, estimating how likely they are to occur, understanding their potential impact, and deciding whether the potential reward justifies taking that risk.

How can I reduce fear when investing?

You can reduce investment-related fear by educating yourself, setting clear financial goals, maintaining an emergency fund, diversifying your investments, and focusing on long-term progress instead of short-term market movements.

Is taking financial risk always a bad idea?

No. Taking appropriate, well-understood risk is often necessary for long-term wealth creation. The key is to take calculated risks that align with your financial goals, time horizon, and risk tolerance.

What is the difference between risk tolerance and risk capacity?

Risk tolerance is your emotional comfort with investment fluctuations. Risk capacity is your financial ability to absorb losses without affecting your lifestyle or long-term goals. Both should be considered before making investment decisions.

Why is diversification important in risk management?

Diversification spreads your investments across different asset classes or sectors, reducing dependence on any single investment. While it cannot eliminate losses or guarantee returns, it helps lower concentration risk and can improve portfolio resilience over the long term.

Disclaimer

This article is for educational and informational purposes only and should not be considered financial, investment, tax, or legal advice. Please consult a qualified financial advisor before making any financial decisions.