How to Recover From a Financial Setback (The Ultimate Guide)

Table of Contents

Facing a financial setback? Learn how to recover from a financial setback, learn practical, India specific steps to recover from job losses and rebuild your finances with confidence.

Life has a way of throwing curveballs right when you least expect them. A sudden job loss, a hospital bill that wipes out your savings, a business that just didn’t work out, or an investment that went south. If you’re reading this because you’re going through a financial setback right now, take a breath. You are not the first person this has happened to, and you won’t be the last.

Here’s the good news. A financial setback is not a life sentence. It’s an event. And like every event, it has a beginning, a middle and an end. This guide walks you through exactly how to get through each stage, with real, India-specific advice you can act on today.

Why Financial Setbacks Happen to Almost Everyone

Before you start blaming yourself, understand this. Financial setbacks don’t discriminate based on income or how smart you are with money. They can be triggered by

- Sudden job loss or salary cuts

- Medical emergencies

- A business that didn’t take off

- Divorce or separation

- Natural disasters

- Bad investment calls

- High interest debt piling up

- Big unplanned expenses like a vehicle repair or home repair

Even seasoned investors and financially disciplined professionals go through rough patches. What separates people who bounce back from those who don’t isn’t luck. It’s how they respond in the first few weeks.

Step 1. Pause Before You Panic

The single biggest mistake people make after a financial hit is making decisions out of fear. You might feel like selling your mutual funds immediately, taking a personal loan at a steep rate, or breaking your fixed deposit without thinking it through.

Don’t.

Give yourself 48 hours before making any big money decision. Ask yourself these questions first.

- What exactly happened, and how big is the actual damage?

- Is this a short-term problem or something that will affect me for years?

- How much cash do I need right now, this month?

- Which of my expenses are truly essential and which can wait?

A calm mind almost always makes a better financial call than a panicked one.

Step 2. Get Brutally Honest About Where You Stand

You cannot fix what you don’t measure. Sit down, preferably with a notebook or a simple spreadsheet, and list out

Income – salary, freelance work, rental income, any side business earnings

Essential expenses – rent or EMI, groceries, electricity and utility bills, insurance premiums, school fees, transport

Debts – credit card outstanding, personal loans, home loan, car loan, and any Buy Now Pay Later dues

Savings and investments – emergency fund, bank balance, mutual funds, PPF, EPF balance, NPS corpus, and other liquid assets

Once the numbers are in front of you, the fog usually clears a little. Most people feel worse in their head than what the actual numbers show.

Step 3. Build a Bare Bones Survival Budget

Forget your regular monthly budget for now. What you need is a survival budget that covers only what keeps your life running.

That typically means rent or home loan EMI, electricity and water, groceries, health insurance premium, and minimum debt payments. Everything else, dining out, OTT subscriptions, that online shopping habit, goes on pause until things stabilise.

This isn’t forever. It’s a temporary seatbelt, not a permanent lifestyle.

Step 4. Talk to Your Lenders Before They Call You

Most people avoid their bank’s calls when they’re struggling to repay a loan. This almost always backfires.

If you think you’ll miss an EMI or credit card payment, reach out to the lender first. Ask about restructuring options, a temporary moratorium, or a revised repayment schedule. Banks and NBFCs in India generally prefer working out a solution over pushing a customer into default, since defaults hurt their books too.

Being proactive here can protect you from penalty charges and steeper damage to your credit score than a missed payment or default would cause, even though a restructured loan may still show up as a flag on your credit report.

Step 5. Stay Far Away From High Interest Debt

When money is tight, quick loan apps and easy credit can look tempting. Be extremely careful here. Many personal loan and credit card products in India carry annual interest rates in the range of 30 to 48 percent, and some instant loan apps charge even more once you account for processing fees and penalties.

Borrowing at these rates to cover a temporary cash crunch can turn a manageable setback into years of debt stress. If you absolutely must borrow, compare the total cost across a few lenders before signing anything.

Step 6. Protect, Don't Deplete, Your Emergency Fund

If you built an emergency fund, this is exactly what it’s for. Use it, but use it wisely. Withdraw only what you genuinely need rather than emptying the entire fund in one go.

If you don’t have one yet, don’t panic about building it while you’re still in crisis mode. Focus on stabilising first. Once your income is steady again, work towards saving three to six months of essential expenses, adjusted to your own situation and job stability.

Step 7. Look for Ways to Bring in Extra Income

Cutting expenses only takes you so far. Bringing in additional income often speeds up recovery much faster.

Freelancing, weekend consulting, online tutoring, selling things you no longer use, or simply picking up gig work for a few months can ease the pressure considerably. Even a modest extra income stream reduces how much you need to dip into savings or credit.

Step 8. Don't Abandon Your SIPs Completely

Here’s something a lot of financial content gets wrong. It tells you to stop all investments the moment things get tough. In reality, if pausing your SIP for a couple of months is what keeps you from taking an expensive loan, that’s a reasonable trade off.

But if you can manage even a reduced SIP amount alongside your essential expenses, keep it running. Consistency in investing matters more than the exact amount, and restarting a paused SIP later is often harder than people expect, both financially and psychologically.

Step 9. Review Your Insurance Once the Dust Settles

Financial setbacks often expose gaps you didn’t know existed. Once you’re past the immediate crisis, check whether your health insurance cover is adequate, whether you have term life cover if someone depends on your income, and whether your vehicle and home insurance are up to date.

A good insurance policy won’t prevent every setback, but it can stop the next one from being as painful.

Step 10. Turn the Setback Into a Lesson

Every financial setback teaches something, if you’re willing to look. Was your emergency fund too small? Did you rely too heavily on one income source? Were your investments too concentrated in one asset?

Answering these honestly helps you build a stronger financial base than the one you had before the setback hit.

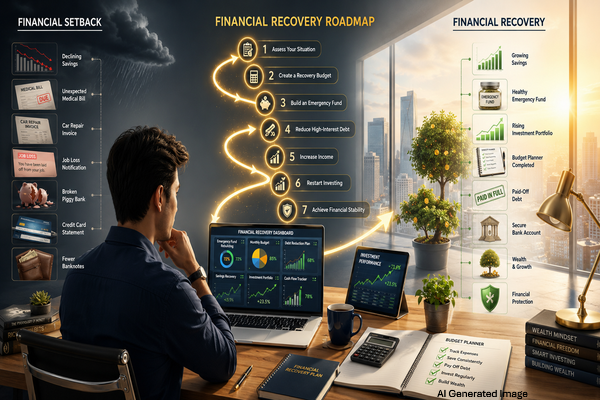

A Simple Recovery Roadmap

First month – stabilize expenses, talk to lenders if needed, get clarity on numbers

Three months – rebuild a small buffer, look for extra income, resume paused SIPs if possible

Six months – strengthen your emergency fund, pay down high interest debt, review insurance

One year – return fully to your long-term financial goals and resume systematic wealth building

Final Thoughts

A financial setback feels enormous when you’re in the middle of it. But it is a chapter, not the whole story. Stay calm, get honest with your numbers, protect your essentials, and rebuild step by step. The professionals and investors who come out stronger after a setback usually aren’t the ones who never stumbled. They’re the ones who kept moving, one deliberate decision at a time.

Recovery isn’t about speed. It’s about direction.