Common Term Insurance Myths That Cost Families Crores

Table of Contents

Discover the truth behind common term insurance myths that cost families crores. Learn why term insurance is affordable, essential, and how misconceptions lead to financial gaps.

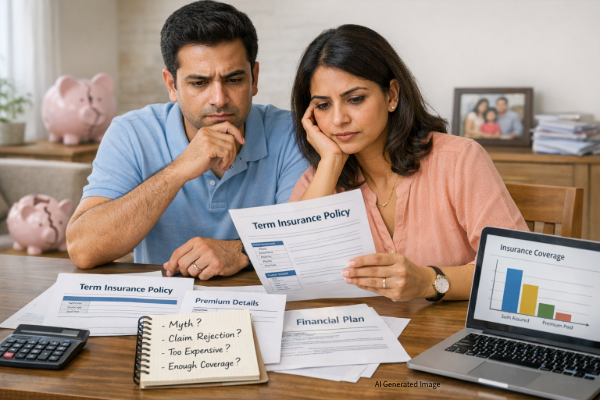

Let me share something that troubles me deeply as a financial advisor. Every week, I meet families who’ve been misled by term insurance myths stories passed down from well-meaning relatives, shared in WhatsApp groups, or worse, advice from people who genuinely believe they’re helping. And you know what breaks my heart? These myths don’t just cause confusion. They cost families crores of rupees in lost protection.

Term insurance isn’t complicated. It’s actually the simplest, most honest form of life insurance you’ll ever find. Pure protection. No gimmicks. No fancy investment promises. Just a straightforward commitment: if something happens to you during the policy term, your family gets the financial security they need to continue living their dreams.

But here’s where things go wrong. Misconceptions about term plans have created a climate of fear, hesitation, and outright misinformation. People delay buying term insurance, choose inadequate coverage, or pick expensive alternatives that drain their savings without providing sufficient protection.

Today, I’m setting the record straight. Let’s talk about the most damaging term insurance myths I encounter myths that have real consequences for real families and more importantly, what the actual truth is.

Myth #1: "Term insurance is too expensive."

Reality: Term insurance is among the most affordable forms of life insurance available in India today.

I’ve seen this myth destroy families’ financial futures more times than I can count. A 30-year-old professional earning ₹8 lakhs annually once told me he couldn’t ‘afford’ term insurance. When I showed him he could get ₹1 crore coverage for roughly ₹800-1,000 per month, he was stunned. That’s less than what most people spend on weekend entertainment or online shopping.

Here’s why term insurance premiums are so reasonable: unlike traditional life insurance plans that bundle insurance with investment, term plans offer pure risk cover. There’s no maturity benefit. No savings component. No fancy cash back features. Just straightforward life protection which means the insurance company can offer substantial coverage at a fraction of the cost.

Think about it this way: would you rather pay ₹10,000 monthly for a policy that gives you ₹25 lakhs coverage plus ‘returns’ at the end, or pay ₹1,000 monthly for ₹1 crore pure term cover? The mathematics speaks for itself. And that extra ₹9,000? Invest it properly, and you’ll build far more wealth than any traditional plan could ever promise.

But here’s the kicker: waiting to buy term insurance costs you exponentially more. Insurance premiums increase with age and declining health. A 25-year-old buying ₹1 crore coverage might pay ₹7,000 annually. Wait until 40? That same coverage could cost ₹18,000-25,000 per year. Over a 25-year policy term, that delay could cost you an additional ₹5-6 lakhs. That’s not ‘saving’ that’s financial self-sabotage.

Myth #2: "I don't need term insurance if I'm young and healthy."

Reality: Being young and healthy is exactly when you need to lock in your term insurance coverage.

Last month, a 28-year-old client came to my office after his friend same age, apparently healthy passed away suddenly from a heart attack. “I thought these things only happened to older people,” he said, visibly shaken. That’s the dangerous illusion our mind creates: we believe tragedy happens to others, never to us.

Life doesn’t wait for you to be ‘ready.’ Accidents don’t check your age before happening. Critical illnesses can strike at any time. And here’s the brutal truth: insurance companies don’t sell policies based on what might happen they sell based on your current health status and risk profile.

When you are young and healthy, insurance companies see you as low risk. That translates to lower premiums and easier approval processes. But develop diabetes, hypertension, or any other chronic condition? Premiums skyrocket. Some conditions might even make you uninsurable.

I’ve seen perfectly healthy 35-year-olds denied term insurance because they developed thyroid issues, or quoted premiums 40-50% higher than standard rates due to borderline blood pressure readings. The time to buy term insurance isn’t when you need it by then, it’s often too late or too expensive. The time to buy is when you don’t think you need it.

Myth #3: "If I survive the policy term, I lose all my money."

Reality: Term insurance is protection, not an investment. You are not ‘losing money’ you are buying peace of mind.

This is hands-down the most frustrating term insurance myth I deal with. People view insurance through an investment lens, which is completely backward. Let me ask you something: do you have car insurance? Health insurance? Home insurance? When your car doesn’t get stolen or your house doesn’t burn down, do you feel like you’ve ‘lost money’ on those premiums?

Of course not. You understand those are protection products. Term insurance works the same way. Every month you pay that premium, you are ensuring your family’s financial security. If you survive the term and I sincerely hope you do celebrate it! You got to live, watch your children grow, achieve your dreams. That’s the whole point.

Now, I know some people still want that ‘money back’ feeling. Fair enough. That’s why insurers offer Return of Premium (ROP) term plans. These refund your premiums if you survive the policy term. But here’s what they don’t advertise: ROP plans cost 2-3 times more than regular term insurance. A 30-year-old paying ₹12,000 annually for a ₹1 crore term plan might pay ₹35,000-40,000 for the same coverage with ROP.

Is that worth it? Let’s do some math. With regular term insurance, you pay ₹12,000 yearly for 30 years = ₹3.6 lakhs total. With ROP, you pay ₹40,000 yearly for 30 years = ₹12 lakhs total. After 30 years, you get that ₹12 lakhs back. But if you’d taken the regular term plan and invested that extra ₹28,000 annually at just 8% returns, you’d have ₹32 lakhs after 30 years. The ‘return of premium’ feature actually costs you ₹20 lakhs in lost opportunity.

Myth #4: "My employer's group cover is enough."

Reality: Employer-provided group insurance is a valuable benefit, but it’s inadequate for comprehensive family protection.

A senior IT professional with a 10-year career came to me after switching jobs. His previous employer provided ₹50 lakhs group term insurance. His new company? Only ₹25 lakhs. He had a home loan of ₹45 lakhs, two children under 10, and no personal term insurance. “I thought I was covered,” he said. That’s when reality hit.

Group insurance has three critical flaws. First, coverage is typically limited often just 2-3 times your annual salary, which rarely matches your family’s actual financial needs. Second, it’s non-portable. Change jobs? Your coverage changes or disappears. Get laid off? You are suddenly uninsured at possibly the worst financial moment of your life. Third, you have zero control. Employers can reduce coverage, change insurers, or eliminate benefits entirely during company restructuring.

Personal term insurance is yours. Completely portable. Fully controlled by you. It doesn’t matter if you switch careers, start a business, take a sabbatical, or retire early your family’s protection remains intact. Treat your group cover as a bonus, not your safety net. Your family’s financial security deserves better than depending on your employer’s goodwill.

Myth #5: "Term insurance isn't necessary if I have savings or other investments."

Reality: Savings and investments are for building wealth. Insurance is for protecting that wealth from catastrophic loss.

I met a successful business owner who’d accumulated ₹2 crore in investments. “Why would I pay for term insurance when I have this corpus?” he asked. Great question. Here’s my answer: What happens if you pass away tomorrow? Your spouse inherits ₹2 crore. Sounds good, right?

Now let’s subtract reality. Business loan: ₹60 lakhs. Home loan: ₹35 lakhs. Children’s education expenses for the next 15 years: ₹80 lakhs conservatively. Household expenses to maintain current lifestyle for 20 years: ₹75 lakhs. Total: ₹2.5 crore. Your ‘adequate’ savings just left your family ₹50 lakhs short, forcing them to downgrade their lifestyle or compromise on children’s education.

And that’s assuming everything goes perfectly. What if your death occurs during a market downturn? That ₹2 crore portfolio might be worth ₹1.4 crore. What if there are medical expenses not covered by health insurance? Emergency liquidating investments often means selling at the worst possible time, destroying years of wealth accumulation.

Term insurance provides instantaneous liquidity. Your family gets the sum assured typically ₹1-2 crore without touching their existing investments, which can continue growing to fund retirement, children’s weddings, or legacy wealth. It’s not either-or. It’s both-and. Savings and insurance serve completely different purposes in a healthy financial plan.

Myth #6: "Term insurance claims are often rejected."

Reality: Reputable insurers in India maintain claim settlement ratios of 95-99%. Most rejections happen due to non-disclosure or fraud, not arbitrary denial.

This myth perpetuates because rejected claims make news. Settled claims don’t. It’s selection bias in action. Yes, IRDAI (Insurance Regulatory and Development Authority of India) data shows some claims get rejected but dig into the reasons, and you’ll find most involve material non-disclosure during policy purchase.

Here’s what actually causes claim rejection: lying about smoking status, hiding pre-existing medical conditions, not disclosing dangerous hobbies, or providing false information about income or lifestyle. Insurance works on the principle of ‘utmost good faith’ both parties must be completely honest. If you misrepresent facts during application, the insurer has every right to reject your claim.

But if you’re honest and transparent? Your claim will be settled. The numbers prove it. Leading insurers like HDFC Life, ICICI Prudential, and Max Life consistently report claim settlement ratios above 98%. These are lakhs of families receiving the financial protection they paid for. So when someone tells you ‘insurance companies never pay claims,’ ask them: where’s the evidence? Because the data says otherwise.

My advice? Be brutally honest during your application. Disclose everything even if you think it’s minor. Insurance companies can handle risk; what they can’t handle is deception. Complete transparency during purchase guarantees smooth claim settlement later.

Myth #7: "Term insurance is only for breadwinners."

Reality: Anyone whose absence would create financial strain for their family needs term insurance.

I’ll never forget the conversation with a homemaker who asked, half-jokingly, “What’s the insurance value of someone who doesn’t earn?” The question broke my heart because it revealed how deeply we undervalue non-salaried contributions to family welfare.

Let’s talk numbers. Who manages the home? Who cooks nutritious meals? Who coordinates children’s schedules? Who provides emotional support and caregiving? If a homemaker passes away, hiring someone to replace even half those services costs ₹30,000-50,000 monthly. Over 10 years, that’s ₹36-60 lakhs. Add the emotional trauma and productivity loss for the surviving spouse, and the financial impact becomes staggering.

Every contributing family member deserves term insurance. If your death would force your family to make financial adjustments hiring help, relocating, changing career plans you need coverage. Period. This applies to working professionals, homemakers, elderly parents who provide childcare, or adult children supporting their parents. Financial contribution isn’t just about salary; it’s about the value you provide.

Myth #8: "All term plans are alike."

Reality: Term insurance products differ significantly in riders, coverage options, and flexibility. Choosing the wrong plan can leave coverage gaps or waste money.

Not all term insurance is created equal. Some policies offer increasing cover options your sum assured grows annually to combat inflation. Others provide critical illness riders that pay out a lump sum if you are diagnosed with specified conditions, even if you survive. Accident benefit riders double or triple your coverage if death occurs due to an accident.

Premium payment structures vary too. Some plans allow single premium payment. Others offer limited pay options where you pay for 10-15 years but stay covered for 30-40 years. Policy terms range from 10 to 40 years or up to age 75-85. Claim settlement reputation, customer service quality, and digital convenience differ vastly between insurers.

Generic ‘cheapest term insurance’ comparisons miss these nuances. A slightly higher premium might buy you significantly better riders, more flexible terms, or an insurer with superior claim settlement processes. Work with a financial advisor who understands your unique situation and can recommend customized coverage rather than generic ‘best term insurance plan’ articles.

Final Takeaway: Why These Myths Are Costing Families Crores

After years in this industry, I can tell you exactly what these term insurance myths cost families:

Delayed purchase means paying 50-100% higher lifelong premiums costing families ₹5-10 lakhs extra over a policy term.

Under-insuring leaves families with insufficient coverage when ₹50 lakhs was needed but only ₹25 lakhs was purchased, creating a ₹25 lakh financial gap at the worst possible moment.

Choosing expensive alternatives like traditional plans or ULIPs instead of pure term insurance means paying 3-5 times more for the same coverage, draining ₹10-15 lakhs from wealth-building opportunities.

Overconfidence in employer coverage or savings creates dangerous protection gaps families forced to liquidate investments during emergencies, destroying years of wealth accumulation.

Term insurance isn’t an expense you reluctantly bear. It’s the foundation of responsible financial planning the cornerstone of your family’s financial safety net. It preserves your family’s standard of living, protects their dreams, and ensures that your absence doesn’t translate into financial devastation.

Life is unpredictable. Financial protection shouldn’t be. Don’t let myths cost your family crores. Make informed decisions. Get adequate coverage. Buy term insurance today, not tomorrow.

Your family deserves that certainty. You deserve the peace of mind knowing they’ll be financially secure no matter what life throws your way. That’s not just smart financial planning it’s love translated into action.

FAQs

How much term insurance cover should I buy?

A practical thumb rule is 10–15 times your annual income, but that’s only a starting point. A better method is the Human Life Value (HLV) approach calculate your outstanding loans, children’s future education costs, daily living expenses for 15–20 years, and subtract existing assets. The final number should comfortably protect your family’s lifestyle.

What is the ideal age to buy term insurance?

What is the maximum term I should choose?

Are term insurance claims really settled smoothly in India?

Yes, provided you disclose all information honestly. Insurers regulated by the Insurance Regulatory and Development Authority of India (IRDAI) publish claim settlement ratios annually. Most leading insurers maintain high settlement ratios, especially when there is full and accurate disclosure at the time of purchase.

What happens if I miss a premium payment?

Most policies offer a grace period (usually 15–30 days). If the premium isn’t paid within this period, the policy may lapse. However, insurers usually allow reinstatement within a specified time, subject to conditions.