Loan Planning Made Easy with an EMI Calculator

Table of Contents

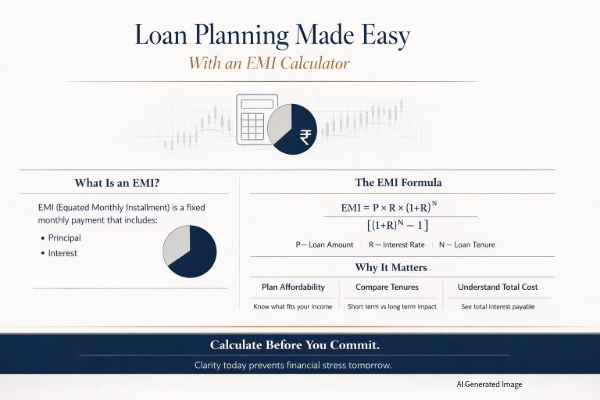

Learn how to use EMI calculator. Loan planning made easy with an EMI calculator. Understand EMI, total interest payable, loan tenure, and the 40% rule to borrow smart and stay stress-free.

Taking a loan is easy. Repaying it comfortably is the real challenge.

Most borrowers spend weeks comparing banks, negotiating interest rates, and waiting anxiously for loan approval. But here is the part they skip: actually checking whether they can afford the monthly repayment without straining their budget. That one blind spot causes more financial stress than any interest rate ever could.

Whether you are planning a home loan, car loan, personal loan, or education loan, an EMI calculator is the one tool that converts confusion into clarity. It takes three simple inputs and shows you exactly what you are getting into before you sign anything.

This guide walks you through how to use an EMI calculator the right way, what numbers you must pay attention to, and how to avoid the mistakes that trap thousands of borrowers every year.

Why You Should Never Take a Loan Without Using an EMI Calculator

1. It Prevents Over-Borrowing

Walk into any bank and the first thing they will tell you is how much loan you are eligible for. That number feels exciting. It is also dangerously misleading.

Eligibility is calculated based on your income and existing liabilities. Affordability is something completely different. It accounts for your actual monthly expenses, investments, insurance premiums, and the financial cushion you need to live without stress.

The right question to ask is not how much loan can I get but how much EMI can I comfortably pay every month. An EMI calculator helps you answer that second question precisely. You enter your comfortable monthly EMI limit and reverse-calculate the safe loan amount, instead of borrowing the maximum and hoping for the best.

2. It Helps You Choose the Right Tenure

Loan tenure is one of the most underrated decisions in loan planning. Many borrowers pick the longest tenure because it gives the lowest EMI. That logic makes sense on paper. In practice, it costs significantly more.

Take a home loan of Rs. 30 lakh at 8.5% interest. opt for a 20-year tenure and your EMI is manageable. Stretch it to 30 years and the EMI drops further, but the total interest you pay increases by lakhs. The EMI calculator shows you this trade-off in seconds, side by side, across multiple tenures.

Once you see those numbers, the decision becomes far easier to make with confidence.

3. It Shows the Real Cost of Interest

Most people focus only on the monthly EMI. Smart borrowers look beyond that. They look at the total interest payable over the entire loan tenure and the total repayment amount, which is the principal plus all the interest combined.

Even a 0.5% difference in interest rate can mean a difference of several lakhs in total repayment over a 20-year home loan. As per RBI guidelines, all regulated lending institutions are required to disclose the annualized percentage rate clearly so borrowers can make an informed comparison. Always read that disclosure and cross-check it using the EMI calculator before finalising any loan.

Step-by-Step: How to Use an EMI Calculator Properly

Step 1: Enter the Loan Amount. Be realistic here. Do not enter the maximum amount the bank is willing to give you. Enter the amount you genuinely need. Borrowing more than required only increases your interest burden without adding any value.

Step 2: Input the Interest Rate. Use the exact rate offered by your bank. Home loan interest rates in India currently range between 8% and 9.5% depending on your credit profile, lender, and loan type. For floating rate loans, use the current rate as a starting point, and run stress-test scenarios as well.

Step 3: Select Loan Tenure. Do not just try one tenure. Compare at least three options, for example 10 years, 15 years, and 20 years, and study how the EMI and total interest change across each.

Step 4: Study These 3 Numbers Carefully. Once the EMI calculator generates results, focus on three things: your monthly EMI, total interest payable over the loan tenure, and total repayment amount. Do not proceed with any loan until you are genuinely comfortable with all three figures.

The 40% EMI Rule (Golden Rule of Loan Planning)

This is the single most practical rule in personal finance: your total monthly EMIs, combining all active loans, should not exceed 35 to 40% of your monthly take-home income.

Say your take-home salary is Rs. 1,00,000 per month. Your total EMI outflow across all loans should ideally stay between Rs. 35,000 and Rs. 40,000. That leaves enough room for household expenses, insurance premiums, SIP investments, emergency savings, and discretionary spending.

Cross this threshold and financial stress becomes almost inevitable. One medical emergency, one month of reduced income, or one unexpected expense and the entire repayment plan starts wobbling. The 40% rule is not conservative. It is just sensible.

Fixed vs Floating Interest Rates: How EMI Calculators Help

A fixed interest rate loan keeps your EMI constant for the agreed fixed period, giving you predictability in monthly budgeting. A floating rate loan, on the other hand, is linked to the lender’s benchmark rate, which moves when the Reserve Bank of India revises its repo rate based on inflation and broader economic conditions.

When the RBI raises the repo rate, lenders typically increase floating loan interest rates, which means your EMI either goes up or your loan tenure gets extended. Both outcomes affect your financial plan.

This is where stress testing with an EMI calculator becomes essential. Before finalising a floating rate loan, simulate three scenarios: the current interest rate, the rate going up by 0.5%, and the rate going up by 1%. If the EMI becomes unaffordable even under the first scenario, reconsider the loan size before you sign.

Real-Life Example: Home Loan Planning

Let us put this into a practical context.

Suppose you are taking a home loan of Rs. 50 lakh at 8.75% interest over a 25-year tenure. Running this through an EMI calculator will show you an approximate monthly EMI of around Rs. 41,000 or more, depending on the exact loan terms and compounding method used by your lender.

But here is the number that really changes how borrowers think: the total interest payable over 25 years. At these terms, you could end up repaying close to Rs. 73 to 75 lakh in interest alone, on top of the Rs. 50 lakh principal. Your total repayment approaches nearly double what you originally borrowed.

Seeing this number does not mean you should avoid taking the loan. It means you should take it with full awareness. Perhaps you increase your down payment. Perhaps you pick a 20-year tenure instead and pay a slightly higher EMI to save a significant amount in total interest. The EMI calculator gives you the data to make that choice.

When Should You Use an EMI Calculator?

An EMI calculator is not just a pre-loan tool. It is useful at multiple stages of your borrowing journey. Use it before applying for any loan, home loan, car loan, or personal loan. Use it when comparing lenders to see how even small differences in interest rates affect total repayment. Use it before a balance transfer to confirm the actual savings after factoring in processing fees on the new loan. And use it when you receive a windfall, such as a bonus or maturity proceeds, and want to decide whether to reduce EMI or reduce tenure through prepayment.

Even if a lender has pre-approved you for a higher loan, always run your own calculation independently. Pre-approval reflects eligibility, not suitability.

Common Mistakes Borrowers Make

Ignoring Processing Fees: Processing fees, legal charges, document costs, and loan insurance premiums all add to your effective borrowing cost. Factor these in when calculating whether a loan is genuinely affordable.

Not Checking Prepayment Charges: Some loans, especially older fixed-rate home loans, carry foreclosure or part-prepayment penalties. Know these charges before planning any prepayment strategy.

Assuming Salary Will Always Increase: A home loan can run for 20 to 30 years. Income levels, job security, and personal circumstances change. Build your repayment plan around a conservative income assumption, not an optimistic one.

Taking the Maximum Eligibility Amount: Just because the bank will lend it does not mean you should borrow it. Eligibility is determined by the lender. Affordability must be determined by you.

How EMI Calculators Help in Prepayment Decisions

If you come into extra money mid-loan, you have two prepayment options: reduce the monthly EMI and keep the same tenure, or keep the EMI the same and reduce the outstanding tenure.

Reducing the tenure almost always saves more total interest. But reducing the EMI improves monthly cash flow, which may be the right choice if other financial obligations have increased. Run both scenarios through the EMI calculator and compare the total interest saved under each option before making a call.

Final Thoughts: Loan Planning Is Risk Management

Loans are not the problem. Poor planning around them is. Every year, borrowers across India struggle not because their interest rates were too high, but because they never sat down and calculated whether the repayment was sustainable in the first place.

An EMI calculator solves that. It is free, takes under five minutes, and gives you three numbers that can completely change how you approach a loan decision: what you can afford, how much total interest you will actually pay, and whether the loan genuinely fits your long-term financial plan.

Before signing any loan agreement in 2026, spend ten minutes with an EMI calculator. Compare tenures. Run stress tests on interest rates. Check your EMI against the 40% rule. Make sure your emergency fund covers at least six months of EMI payments.

A loan taken with clear eyes is a financial tool. A loan taken on assumptions is a financial risk. The difference between the two is planning, and the EMI calculator is where that planning begins.

FAQs

What is an EMI in simple terms?

Is an EMI calculator accurate?

Yes. EMI calculators use a standard mathematical formula used by banks and NBFCs. However, final EMI may slightly vary due to:

- Processing fees

- Insurance premiums

- Interest rate changes (for floating loans)

- Exact disbursement date

Always confirm the final schedule from your lender.

How much of my salary should go toward EMIs

Does increasing loan tenure reduce EMI?

Yes. A longer tenure reduces monthly EMI but increases total interest paid.

Shorter tenure increases EMI but reduces total interest burden.

Example: A 30-year home loan can cost significantly more in total interest compared to a 20-year loan.