What to Do If You Have No Emergency Fund

Table of Contents

No emergency fund? Learn how to build one step by step. This practical recovery plan covers what to do if you have no emergency fund.

Unexpected expenses don’t send invitations.

One day everything is fine. Then your roof starts leaking, your bike breaks down on the highway, or you get a medical bill you weren’t expecting. If you have no emergency fund in place, even a small financial shock can send you spiraling into debt. And before you know it, you are paying 36% interest on a credit card to cover an expense that cost you only a few thousand rupees.

The good news? You can fix this. It doesn’t matter if you Are starting from zero. Building an emergency fund is less about how much money you earn and more about making a decision to start. This guide walks you through exactly what to do, step by step.

Why an Emergency Fund Is Non-Negotiable

An emergency fund is money kept aside specifically for unplanned expenses. Not for a holiday you’ve been planning. Not for a gadget upgrade. Only for genuine emergencies like job loss, a medical bill, or a sudden home repair.

Most financial planners recommend saving 3 to 6 months of essential living expenses. That covers rent or home loan EMI, groceries, utilities, insurance premiums, and your basic transportation costs.

Why 3 to 6 months? Because that’s roughly how long it takes to find a new job, recover from a health setback, or stabilize after an income disruption. According to the Periodic Labour Force Survey published by India’s Ministry of Statistics and Program Implementation, employment volatility remains a persistent reality, particularly in informal and contract-based jobs. Income disruption is not rare in India. It’s predictable.

An emergency fund is not a luxury. It is the base layer of any sound personal finance plan.

Step 1: Don't Feel Guilty. Take Control.

Before anything else, stop beating yourself up. Millions of Indians are in the same position. A 2023 report by the Reserve Bank of India highlighted that a large portion of Indian households have limited liquid financial savings, with wealth concentrated in physical assets like gold and real estate rather than easily accessible funds.

Guilt doesn’t build your emergency fund. Action does. Shift your focus from what you haven’t done to what you can start doing in the next 30 days. That mental shift alone changes everything.

Step 2: Calculate Your Survival Number

You can’t build an emergency fund without knowing exactly how much you need. So the first practical step is to calculate your bare-bones monthly expense, which is the minimum you need to survive without any extras.

Your survival number includes only these:

- Rent or home loan EMI

- Groceries and cooking gas

- Electricity, water, and mobile recharge

- School fees if applicable

- Health or life insurance premiums

- Basic transportation

Everything else, including dining out, streaming subscriptions, and online shopping, gets removed from this calculation entirely.

Here’s a simple example: If your essential monthly expenses total Rs. 25,000, your first emergency fund target is Rs. 75,000. That is three months of coverage. It’s not a dream number. It’s your real safety net.

Even Rs. 10,000 sitting in a separate account is better than zero. Start there if you have to.

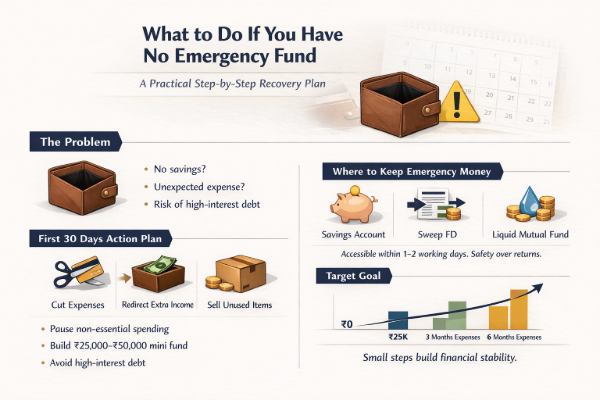

Step 3: Create Immediate Liquidity (Within 30 Days)

If your savings balance is sitting at zero, the goal for the first 30 days is simple: create some cash, fast.

Cut non-essential spending aggressively for 60 to 90 days. Yes, that means eating at home, and skipping weekend outings for a short period. Temporary discomfort in exchange for permanent financial stability is a trade worth making.

Redirect any windfalls directly into your emergency savings. Tax refunds, freelance payments, bonuses from work, and even cash gifts should go straight into this fund right now. No exceptions.

You can also sell idle assets you no longer need. Old electronics, unused gym equipment, jewelry collecting dust in a drawer. Convert these into liquidity. You may be surprised how quickly a few small sales add up to Rs. 5,000 or Rs. 10,000.

Step 4: Protect Yourself From High-Interest Debt

Without an emergency fund, the natural reflex when something goes wrong is to reach for a credit card or take a personal loan. This is exactly where people get stuck.

Credit card interest rates in India typically range between 30% and 45% annually, depending on the bank and the card. Personal loan rates, while lower, still range from 10% to 24% depending on your credit profile, according to RBI data on retail lending trends.

If an emergency does hit before you’ve built your fund, try negotiating the bill first. Many hospitals in India allow staggered payments. Lenders can restructure your EMI if you contact them early. These options are available but people rarely use them because they don’t ask.

Debt should always be your last resort during an emergency, not your first reaction.

Step 5: Start a Mini Emergency Fund First

A lot of people never start because they’re overwhelmed by the idea of saving 6 months of expenses. Don’t do that to yourself. Instead, set a starter emergency fund goal of Rs. 25,000 to Rs. 50,000 first.

This smaller buffer handles the most common emergencies: a minor medical expense, a broken appliance, a temporary gap in income. It won’t cover everything, but it will stop you from going into debt over something small.

Once you hit that milestone, aim for 3 months of expenses. Then push for 6. Small wins build the momentum that keeps you going.

Step 6: Where Should You Keep Emergency Money?

Your emergency fund is not an investment. Stop thinking about returns and start thinking about access and safety.

The best places to park your emergency fund in India include:

- A high-interest savings account with a digital bank or small finance bank

- A sweep-in fixed deposit, which automatically moves excess savings into an FD while staying liquid

- Liquid mutual funds, which invest in short-term money market instruments with maturities up to 91 days as per SEBI regulations, and are relatively low risk compared to equity funds

Avoid stocks, cryptocurrency, or any product with a lock-in period. Your emergency fund must be accessible within 24 to 48 hours. Period.

Also note: liquid mutual funds, while low risk, are not risk-free. Choose only reputed fund houses with a clean track record.

Step 7: Automate the Habit

Waiting until there’s money left over at the end of the month never works. What’s left over is usually nothing, or close to nothing.

Instead, set up an automatic transfer on the day your salary arrives. Even 10% of your monthly income going into a separate emergency savings account, without you having to think about it, is how this habit sticks.

Every time your income goes up, increase the auto-transfer amount. Treat your emergency fund contribution exactly like you treat your rent or EMI. It’s not optional. It’s a fixed expense.

Step 8: What If You Lose Your Job Before Building One?

If you lose your income before your emergency fund is in place, move quickly.

The first thing to do is cut expenses down to survival mode immediately. Every rupee saved is a rupee that extends your runway. Contact your lenders proactively before you miss an EMI, not after. Banks and NBFCs often have restructuring options, but only for customers who communicate early.

Also check your EPF balance. The Employees’ Provident Fund Organization (EPFO) permits partial withdrawals under specific conditions, including a period of unemployment. As per EPFO rules, if you have been unemployed for one month, you can withdraw up to 75% of your EPF balance; after two months, the remaining 25% becomes eligible. This can serve as a short-term buffer while you get back on your feet. However, treat this as an emergency measure, not a substitute for building the habit of saving.

Step 9: Increase Income Alongside Savings

Here’s something that most emergency fund guides don’t say clearly: this is often as much an income problem as a savings problem.

If your current income barely covers your essentials, saving 10% is genuinely hard. So while you cut expenses and automate savings, actively look for ways to bring in more money. Freelancing on weekends. Online tutoring. Consulting in your area of expertise. Even Rs. 5,000 extra per month means Rs. 60,000 more in a year, which is a significant emergency fund for most households in India.

Upskilling in your current field can also lead to a faster salary increase. The income side of the equation matters just as much as the expense side.

Common Mistakes to Avoid

A few things that people get wrong when building an emergency fund:

- Investing emergency money in equity markets. The value can drop 30% right when you need it most.

- Using the fund for a planned vacation or purchase. That’s not an emergency.

- Keeping it in cash at home. It earns nothing and gets spent on small things without you noticing.

- Chasing high returns instead of prioritizing accessibility. Emergency money is not an investment vehicle.

- Ignoring inflation. Make sure your fund grows over time as your monthly expenses rise.

How Long Will It Take to Build One?

Longer than you’d like, and faster than you think, if you are consistent.

If you save Rs. 5,000 per month, you will have Rs. 60,000 in 12 months. If you save Rs. 10,000 per month, you will cross Rs. 1.2 lakh in a year. For someone with monthly expenses of Rs. 25,000, that’s already 3 to nearly 5 months of emergency coverage.

Consistency beats the amount every single time. A person saving Rs. 3,000 per month without fail will be far better off in two years than someone who saves Rs. 15,000 for two months and then stops.

Final Thoughts: Stability Before Strategy

Before you open a Zerodha account. Before you buy a second property. Before you put money into any mutual fund or investment scheme, build your emergency fund.

It is the foundation everything else sits on. Without it, one bad month can undo years of financial progress. With it, you can take calculated risks, make better decisions, and sleep a whole lot better at night.

If you currently have no emergency fund, start today. Transfer Rs. 1,000 into a separate savings account right now. Set a reminder to do it again next week.

The goal is not perfection. The goal is protection.

FAQs

How much emergency fund should I have in India?

Can I use a credit card instead of an emergency fund?

Should emergency funds be invested?

How fast should I build an emergency fund?

As fast as possible without taking new debt. Start with a small target, then scale.