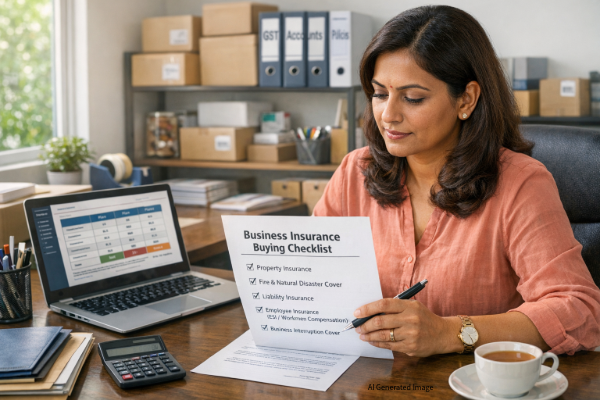

Business Insurance Buying Checklist for Indian Entrepreneurs (2026 Edition)

Table of Contents

Planning to buy business insurance in India? Use this Business insurance buying checklist 2026 to choose the right coverage, stay legally complaint, and protect your business from financial risks. Ideal for SMEs and startups.

Running a business in India takes serious commitment, and the risks that come with it are just as real as the rewards. Whether you are a first-generation entrepreneur setting up a tech startup in Bengaluru, a manufacturer in Pune, or a retailer in Delhi, unexpected events can take a significant financial toll on your enterprise if you are not prepared. Fire, floods, employee accidents, cyberattacks, or a client dispute can wipe out months of hard work overnight.

This is exactly why business insurance in India has become one of the most important financial tools for Indian entrepreneurs in 2026. It is not just about ticking a compliance box. It is about genuinely protecting everything you have built. If you are about to buy a business insurance policy or reviewing your existing coverage, this checklist will walk you through every important step, in plain and practical terms.

1. Understand Your Business Risks and Needs

The first thing you should do before reaching out to any insurance company is take a hard look at your own business. Not all businesses face the same risks, and buying a policy without understanding your exposure is like buying a raincoat when you need sunscreen.

Start by listing down the nature of your business operations, whether you own or rent your premises, the kind of assets you hold (machinery, inventory, office equipment), how many employees work for you, and whether your business has direct customer or third-party interaction. A logistics company will have very different insurance needs compared to a graphic design firm or a food processing unit.

The type of clients you serve also matters. If you offer professional services to corporates or individuals who could hold you liable for any financial loss caused by your advice or deliverables, your exposure is significantly higher than a purely product-based business.

Practical Step: List your risks under four broad heads: property, liability, business interruption, and employee-related claims. This exercise alone will make every subsequent step in your business insurance buying process sharper and more focused.

2. Know the Key Types of Business Insurance in India

The Indian insurance market, regulated by the Insurance Regulatory and Development Authority of India (IRDAI), offers a wide range of business insurance products. Here is a breakdown of the most important ones every Indian entrepreneur should know:

Property and Asset Insurance

This type of policy covers your physical business assets such as the building, stock in trade, plant and machinery, and office furniture against risks like fire, floods, earthquakes, burglary, and riot. The Standard Fire and Special Perils Policy is the most commonly used property insurance product in India for businesses. If your business holds significant physical assets, this is non-negotiable.

Public and Product Liability Insurance

If a customer, vendor, or any third party suffers bodily injury or property damage because of your business operations or your products, you could be held legally and financially responsible. Public liability insurance covers your legal defense costs and any compensation awarded. For manufacturing businesses, product liability insurance is equally important and covers claims arising from defective products.

Professional Indemnity or Errors and Omissions Insurance

This is a must-have for consultants, IT professionals, architects, chartered accountants, and any service-based business where a client can claim financial loss due to errors, omissions, or negligence in your professional work. In India, this type of business insurance is gaining significant traction as more entrepreneurs enter the services and knowledge economy.

Business Interruption Insurance

Imagine your office suffers a severe flood and you cannot operate for three months. Your revenue stops, but your rent, salaries, and loan EMIs do not. Business interruption insurance covers your fixed ongoing costs and loss of profit during the period your business cannot operate due to a covered peril. Many Indian SMEs overlook this policy and end up in serious financial trouble following natural disasters.

Workers Compensation and Statutory Employee Cover

The Employees Compensation Act, 1923 makes it mandatory for most employers in India to compensate workers for injuries or death arising out of employment. Workmen Compensation Insurance fulfills this legal obligation while also protecting you from financial liability in case of workplace accidents.

Commercial Vehicle Insurance

Under the Motor Vehicles Act, 1988, third-party motor insurance is mandatory for every vehicle on Indian roads, including commercial vehicles. If your business owns delivery vans, trucks, or company cars, you need a commercial vehicle insurance policy with at minimum third-party liability coverage.

Cyber Liability Insurance

With businesses storing increasing amounts of customer data online and relying heavily on digital infrastructure, cyber liability insurance has become one of the fastest-growing segments of business insurance in India. This policy covers financial losses arising from data breaches, ransomware attacks, phishing incidents, and associated legal costs. In 2024, India ranked among the top targets for cybercrime globally, making this coverage highly relevant for any digitally active business.

3. Conduct a Thorough Policy Review

Once you have shortlisted a few policies, do not just scan the brochure and sign on the dotted line. The actual policy wordings, which insurers are legally required to share with you, contain the fine print that determines whether you will actually get paid when you file a claim.

Pay close attention to the scope of coverage and, more importantly, the exclusions. Common exclusions in business insurance policies in India include damage due to gradual deterioration, intentional acts, war, and certain natural catastrophes unless specifically added. Also check sub-limits (which cap payouts for specific items), deductibles (the amount you bear before the insurer pays), and waiting periods if any.

Practical Step: Read the policy wording alongside the policy schedule. If any clause is unclear, ask for a written clarification from the insurer or broker before you pay the premium.

4. Compare Quotes and Insurer Credentials

India has 25 non-life insurance companies as of 2025, including public sector giants like New India Assurance and United India Insurance, as well as private players like HDFC Ergo, ICICI Lombard, and Bajaj Allianz. The range of products and premiums across these insurers can vary significantly.

When comparing quotes for business insurance, do not let a lower premium be the only deciding factor. Look at the insurer’s claim settlement ratio, which is published annually by IRDAI. A higher ratio reflects a better track record of honoring claims. Also check the insurer’s solvency ratio, their after-sales service reputation, and turnaround time on claim settlement. A policy that is 10% cheaper but takes three months to settle your claim is a bad deal for any business.

5. Ensure Compliance with Indian Laws

Certain business insurance covers are not optional in India. They are a legal requirement, and non-compliance can attract penalties, legal action, or business closure orders depending on your industry.

- Workmen Compensation Insurance: Mandatory under the Employees Compensation Act, 1923 for most employers.

- Third-Party Motor Insurance: Mandatory under the Motor Vehicles Act, 1988 for every business vehicle.

- Public Liability Insurance: Mandatory under the Public Liability Insurance Act, 1991 for businesses handling hazardous substances.

- Certain licensed sectors such as hospitals, pharma companies, and hazardous goods dealers may also have sector-specific insurance requirements under applicable regulations.

Before finalizing your business insurance portfolio, consult an IRDAI-licensed broker or a legal advisor to make sure you are fully compliant with all applicable regulations.

6. Factor in Add-Ons and Extensions

Standard business insurance policies cover the core risks, but they often leave gaps that are equally important for your specific industry. Add-ons, also known as riders or endorsements, allow you to plug these gaps without purchasing an entirely separate policy.

Some useful add-ons and extensions to consider for business insurance in India include equipment breakdown coverage, loss of documents, cyber risk riders on property policies, consequential business interruption loss, Directors and Officers (D&O) liability for companies with a board, and contractual liability extensions. In 2026, several Indian insurers are offering modular or pay-as-you-go business insurance structures, which are particularly useful for startups and growing SMEs who need flexibility as their risk profile changes.

7. Plan for Future Business Growth

The business insurance policy that works perfectly for your company today may leave you seriously underinsured two years down the line. As your business grows, its risk exposure changes. You hire more people, acquire more assets, enter new markets, and take on bigger clients with more demanding contracts.

Make sure the policies you choose allow for mid-term upward revisions to your sum insured. Set a calendar reminder to review your business insurance coverage at least once a year, and definitely after any major business change such as a new product launch, office expansion, significant revenue growth, or a shift in your business model. Underinsurance is one of the most common and costly mistakes Indian business owners make with commercial insurance.

8. Document and Digitize Your Insurance Records

This is an area where many Indian entrepreneurs fall short, especially small business owners who handle insurance informally. A misplaced policy document or an expired renewal notice can cost you enormously when you actually need to file a claim.

Maintain a dedicated insurance folder, both physical and digital, that includes all policy documents and their schedules, endorsement copies, premium payment receipts, previous claim records, and broker contact details. You can use cloud storage platforms or even a secure email folder for this purpose. Having everything organized means faster claim filing and fewer disputes with the insurer.

9. Consider Tax Benefits

Business insurance premiums paid by a company or a self-employed individual are generally allowed as a deductible business expense under the Income Tax Act, 1961 in India, subject to conditions and the nature of the policy. This means buying the right business insurance not only protects your enterprise but also reduces your taxable income.

For example, premiums paid for fire insurance, public liability insurance, professional indemnity, and workmen compensation are typically deductible as business expenses. However, it is always advisable to consult your Chartered Accountant to understand the exact treatment applicable to your situation and ensure maximum tax efficiency while maintaining adequate coverage.

10. Re-Evaluate Regularly and Engage an Expert

Business insurance is not a one-time purchase. The risk landscape in India changes constantly. New regulations are introduced, cyber threats become more sophisticated, natural disasters increase in frequency, and new industries emerge with unique liability profiles.

Make it a practice to sit with an IRDAI-licensed insurance broker at least once a year for a structured review of your entire business insurance portfolio. A good broker, unlike a tied agent who represents only one company, can compare products across multiple insurers and give you genuinely unbiased advice. They can also help with claim advocacy, which is invaluable when you are in the middle of running a business and dealing with a loss simultaneously.

Practical Step: IRDAI maintains a public register of licensed brokers on its website at irdai.gov.in. Always verify your broker’s license before engaging them for your business insurance needs.

Final Thoughts

Business insurance in India is no longer just a line item in your annual expenses. For any serious entrepreneur, it is a strategic safety net that keeps your business standing when the unexpected strikes. The Indian insurance sector has matured considerably, and the range of products available to SMEs and startups today is more comprehensive than ever before.

By following this business insurance buying checklist, you are not just protecting your assets. You are making a deliberate, informed decision to safeguard your employees, your clients, your financial stability, and your long-term growth. Take the time to do it right, and your future self will thank you for it.

FAQs

What is the most important business insurance for Indian entrepreneurs?

There is no single “most important” policy it depends on your business type. However, most Indian businesses should consider:

- Property insurance

- Public liability insurance

- Workers’ compensation (if you have employees)

- Commercial vehicle insurance (if vehicles are used)

For service businesses, professional indemnity is crucial. For digital businesses, cyber insurance is becoming essential in 2026.

Is business insurance mandatory in India?

Some types are legally mandatory:

- Commercial vehicle insurance under the Motor Vehicles Act

- Employees’ Compensation insurance if you have workers (as per Employees’ Compensation Act)

- Certain industries may require public liability coverage

Other policies are optional but highly recommended for financial protection.

How much does business insurance cost in India?

The cost depends on:

- Nature of business

- Annual turnover

- Asset value

- Risk exposure

- Coverage limits and add-ons

For small businesses, premiums can start from a few thousand rupees per year, but comprehensive coverage may cost more depending on risk size.

What is covered under business interruption insurance?

Typically, insurers may ask for:

- Business registration documents (GST, MSME, incorporation certificate)

- PAN and KYC details

- Asset valuation details

- Revenue information

- Employee details (for workers’ compensation)

Requirements may vary based on the insurer and policy type.

What documents are required to buy business insurance?

Business interruption insurance generally covers:

- Loss of income due to covered damage (like fire or flood)

- Fixed operating expenses (rent, salaries)

- Temporary relocation costs

It usually applies only if physical damage triggers the interruption, so policy wording must be reviewed carefully.

What is not covered under business insurance?

Common exclusions may include:

- Intentional damage

- Wear and tear

- War and nuclear risks

- Undisclosed risks

- Cyber risks (unless specifically covered)

Always read the exclusions section before purchasing.