Why Your Salary Feels Less Every Year (Even Without Inflation Talk)

Table of Contents

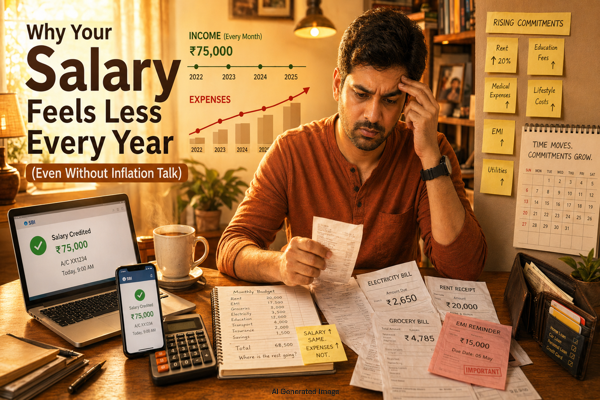

Discover why your salary feels less every year. your salary keeps rising but your account tells a different story. Here is the real structural reason your salary feels less every year, explained with Indian examples, verified formulas, and a practical reset plan.

Your salary went up. Your stress didn’t go down. That’s not a coincidence.

Most people pin it on inflation and move on. But even if prices stayed perfectly stable, millions of salaried Indians would still feel financially squeezed every single month. This is not just a feeling you should brush off. It is a structural money problem, and it gets worse the longer you leave it unaddressed.

Let’s break it down with real numbers, honest frameworks, and relatable Indian examples so you can see exactly what is happening to your money every month.

1. Lifestyle Creep - The 10% Rule That Eats Your Raise

Say your salary in Year 1 is Rs. 50,000 per month. You get a standard 10% increment. You are now at Rs. 55,000. Feels good.

Here is what quietly follows without you planning any of it:

Better apartment rent: +Rs. 2,000. More Swiggy and Zomato orders: +Rs. 1,500. New OTT subscriptions: +Rs. 500. A couple of weekend trips: +Rs. 1,000.

That is Rs. 5,000 gone. Your raise is gone.

The formula is simple but brutal:

Income Growth – Lifestyle Growth = Real Progress

If your income grows by 10% but your lifestyle grows by 8 to 12%, your effective surplus stays flat. Financial planners call this lifestyle creep. It is the first and most common reason your salary feels less every year, yet most people never even notice it happening to them.

2. Fixed Expense Ratio (FER) - The Hidden Pressure Metric

Most people have never heard of this metric. But it quietly explains why some people feel comfortable on Rs. 80,000 a month while others feel completely stretched at the same salary.

FER = Fixed Expenses / Net Income

Here is a real-world Indian example:

Salary: Rs. 80,000. Rent: Rs. 25,000. EMI: Rs. 15,000. Insurance: Rs. 3,000. School fees: Rs. 7,000. Total Fixed Expenses: Rs. 50,000.

FER = 50,000 / 80,000 = 62.5%

As a general guideline used across personal finance:

Below 40% means you are comfortable. 40% to 60% is manageable. Above 60% puts you in the financial stress zone.

At 62.5%, you are already in the red zone before you spend a single rupee on food or petrol. Even if your salary increases next month, a high FER will make you feel financially tight regardless. The number goes up. The pressure stays the same.

3. The "Disappearing Increment" Effect

You get a Rs. 10,000 raise. It sounds solid. Here is exactly where it goes:

Tax impact (approximately 10% to 20% depending on your tax regime and income slab): -Rs. 1,000 to Rs. 2,000. Lifestyle upgrade: -Rs. 4,000. Higher EMI or a new financial commitment: -Rs. 3,000.

What is potentially left: Rs. 1,000 or less.

And that often ends up on a restaurant tab or an impulse purchase before the month is over.

To give context on the tax piece: under India’s new default tax regime for FY 2025-26, a salaried person earning around Rs. 80,000 per month (Rs. 9.6 lakh annually) falls in the 10% marginal slab. Under the old tax regime, the same income falls in the 20% slab. Which regime you are on changes how much of your raise you keep. Either way, the government takes a portion before you even see it.

This is the disappearing increment effect. Your raise exists on paper. You never actually feel it.

4. Cash Flow Illusion - Why You Feel Broke Despite Saving

Here is a scenario many working professionals in India will recognize immediately:

Salary: Rs. 1,00,000. SIPs and investments: Rs. 25,000. Monthly expenses: Rs. 70,000. What is left in the bank at month-end: Rs. 5,000.

Your brain sees Rs. 5,000 and panics. But look at what is actually happening. You are building Rs. 25,000 in wealth every single month.

The framework to lock in:

Net Worth Growth matters far more than Bank Balance

If your mutual funds, provident fund, and equity investments are growing consistently, you are progressing financially, even when your savings account looks thin on the 28th of the month. The feeling of being broke and actually being broke are two very different things. Learning to tell them apart is one of the most valuable shifts in personal finance thinking you can make.

5. Responsibility Multiplier - Same Salary, More Jobs

A few years ago, your salary belonged mostly to you. Today, it is doing multiple jobs before you even see your bank notification.

Earlier (single, minimal expenses):

Savings rate: around 30%. Freedom of choice: high.

Now (same or higher salary):

Family support: Rs. 10,000. Home loan EMI: Rs. 20,000. Insurance and medical costs: Rs. 5,000. Total new obligations: Rs. 35,000.

Your salary did not shrink. Your money got divided across more people and more responsibilities. This is the responsibility multiplier at work. It is one of the most overlooked reasons your salary feels less every year, and almost no mainstream financial content in India talks about it directly.

6. The "Enough Number" Gap (ENG)

This is where psychology meets personal finance, and it is surprisingly powerful in explaining long-term financial dissatisfaction.

ENG = Desired Lifestyle Cost – Current Income Allocation Comfort

Example: Your comfortable lifestyle cost expectation is Rs. 1.5 lakh per month. Your current income is Rs. 1 lakh. The gap is Rs. 50,000.

Even if you are objectively doing well, that gap creates a steady hum of financial anxiety in the background. Academic research published in the Annual Review of Economics defines this as the “income aspirations gap” – the distance between what a person desires and what they currently earn. Studies consistently show that when this gap is too wide, it is linked to reduced financial motivation and lower life satisfaction, even among people who are saving and investing responsibly. The number feels insufficient not because it is, but because the mental benchmark keeps moving up faster than income does.

7. Savings Rate vs Income Growth (The Real Wealth Indicator)

Most people fixate on their salary figure. People who actually build wealth track their savings rate.

Savings Rate = (Savings / Income) x 100

Year – 2022 – Salary – Rs. 50,000 – Savings – Rs. 10,000 – Savings Rate – 20%

Year – 2024 – Salary – Rs. 80,000 – Rs. 12,000 – Savings Rate – 15%

Salary went up by 60%. Savings rate dropped by 25%. You are earning more and building wealth more slowly at the same time.

This is the core reason it feels like you are standing still. A higher income with a shrinking savings rate is not progress, it is a treadmill. The math of compounding rewards consistency of savings far more than size of salary. That is why two people can retire very differently on very similar incomes.

8. Expense Elasticity - Why Spending Expands Automatically

Think of your expenses like a gas. They expand to fill whatever financial space is available.

Elastic expenses that rise fast the moment income grows: food delivery, online shopping, entertainment, and travel. Inelastic expenses that rise slowly: rent, EMIs, school fees, and insurance.

The moment your income goes up, elastic expenses jump immediately. Inelastic ones creep up over the following months. So you never actually experience that window of “extra cash.” It evaporates before you can redirect it.

This pattern follows what C. Northcote Parkinson described as his Second Law: “Expenditures rise to meet income.” Originally an observation about work and time, Parkinson explicitly extended it to personal finance. No matter the income, people naturally find ways to spend all of it. The law has been widely cited in management and behavioral economics for decades.

Practical Financial Reset (Actionable Framework)

Reading about the problem is one thing. Here is what you actually do about it.

1. Cap Lifestyle Growth to 50% of Increment

If your raise is Rs. 10,000, spend only Rs. 5,000 of it on lifestyle improvements. Save or invest the other half. You still get to upgrade your life, just not at the full cost of your increment.

2. Keep Fixed Expense Ratio Below 50%

Before signing a higher-rent lease or taking on a new EMI, calculate your FER first. If that commitment pushes you above 50%, wait. Delaying financial commitments strategically is not sacrifice. It is discipline.

3. Follow the 30-30-30-10 Framework

This is a practical adaptation of common budgeting principles, not a rigid financial rule – think of it as a starting template:

- 30% for fixed expenses (rent, EMIs, insurance)

- 30% for lifestyle spending (food, travel, shopping)

- 30% for investments (SIPs, EPF top-up, stocks)

- 10% for buffer or unplanned spending

Adjust the percentages to your situation, but the logic holds: ring-fence investments before lifestyle gets first claim.

4. Track Net Worth Monthly, Not Just Salary

Build a simple monthly tracker. Include mutual funds, EPF balance, equity, and cash. Checking it once a month shifts your mental focus from “I only have Rs. 5,000 left” to “my net worth grew by Rs. 28,000 this month.” That shift in perspective is worth more than a pay raise in terms of financial behavior.

5. Run a “1-Year Expense Audit”

Once a year, ask two honest questions. What new expenses did I add this year? Which ones actually improved my quality of life?

Cut the ones that didn’t. That unused gym membership, the streaming service you open twice a month, the premium upgrade nobody in the house asked for. Small cuts add up to thousands of rupees annually, and redirecting them to SIPs creates compounding wealth.

Final Thought

Your salary does not feel less because it is small.

It feels less because your cost structure keeps expanding quietly, your money now carries more responsibilities than it used to, your savings are growing in the background where you cannot see them, and your lifestyle expectations are rising faster than your income.

None of this is about earning more. All of it is about understanding where the money is going.

Fix the structure, and your current salary will start feeling very different. Not because it changed, but because you are finally in control of it.

FAQs

What is the ideal savings rate?

At least 20–30% of your income. Higher if you start late.

Why do I feel broke even when I save?

Because savings are not visible daily, but expenses are.

What is the biggest mistake people make after a salary hike?

Increasing lifestyle expenses immediately.

Disclaimer

This article is for educational purposes only and does not constitute financial advice. Please consult a qualified financial advisor before making financial decisions.