How Social Media is Secretly Making You Poorer (Hidden Spending Traps)

Discover how social media is secretly making you poorer. Learn the hidden psychological traps that drain your wallet and practical steps to protect your money

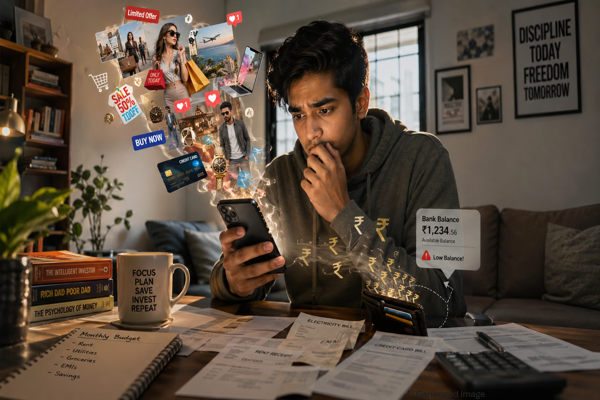

You open your phone for five minutes.

Forty-five minutes later, you close it with two items sitting in your cart.

That is not a coincidence.

Social media and spending habits are far more connected than most people realize. These platforms are not just entertainment. They are carefully engineered environments built to influence how you think, how you feel, and most importantly, how you spend.

The scary part? It does not look like advertising. It looks like a friend’s vacation photo. It looks like a review from someone you trust. It looks like a sale that ends in 3 hours.

You may not feel the damage today. But across weeks and months, social media quietly chips away at your ability to save, invest, and build real wealth.

Let us break down exactly how it happens and what you can do about it.

1. The Comparison Trap: Why You Feel Behind

Think about what you actually see on social media.

Vacations, not the EMIs that paid for them. New cars, not the loans behind them. Fancy dinners, not the credit card bill that followed.

Nobody posts a photo of their debt. Nobody shares a story about skipping dinner out to hit a savings goal. You only see the highlight reel, and over time, your brain starts treating that highlight reel as normal life.

This is not just casual observation. Research in behavioral psychology consistently shows that upward social comparison — measuring yourself against people who appear to be doing better — increases dissatisfaction and drives higher consumption. A 2013 study by Ethan Kross et al. at the University of Michigan, published in PLOS ONE, found that the more people used Facebook over a two-week period, the more their life satisfaction declined over time.

When you feel behind, you spend to catch up.

Financial Impact:

- Lifestyle upgrades you cannot yet afford

- A reduced savings rate

- Money spent to match a social image that was never real to begin with

2. Influencer Marketing: Ads That Don't Feel Like Ads

“My daily essentials.”

“Things I genuinely swear by.”

“You actually need this in your life.”

That content you just watched? There is a very good chance someone paid for you to see it.

Influencer marketing is one of the fastest-growing advertising formats in the world precisely because it works. According to Statista, the global influencer marketing industry was valued at approximately $21.1 billion in 2023 and has more than doubled in value since 2019.

The reason it works so well is trust and relatability. You are not watching a TV commercial. You are watching someone who feels like a peer tell you about something they love. That lowers your defenses and increases the chance you reach for your wallet. This is a core principle of behavioral economics: perceived authenticity significantly increases purchasing intent.

Financial Impact:

- Impulse purchases on items you had no plan to buy

- Spending on trends rather than genuine value

- A budget quietly shaped by someone else’s sponsored agenda

3. Instant Gratification Is Rewiring Your Money Habits

Short videos. Quick reactions. Instant dopamine.

The structure of modern social media is built around speed and immediate reward. Scroll, like, share, repeat. The faster the feedback loop, the more your brain adapts to expecting instant satisfaction.

The connection between delayed gratification and financial outcomes has been studied extensively. Psychologist Walter Mischel’s famous Stanford marshmallow experiment, conducted in 1970, showed that children who waited for a larger reward tended to have better outcomes later in life. Separate longitudinal research, including a study of 1,000 New Zealanders tracked from birth to age 32, found that lower self-control in childhood was associated with greater financial difficulties in adulthood. That said, more recent research — including a 2018 replication study — suggests these outcomes are also shaped heavily by socioeconomic background, so willpower alone is not the full story. The broader point remains: social media, by design, trains the brain toward immediacy, not patience.

Instead of asking yourself, “Do I actually need this?” you start asking, “Why not just buy it today?”

Financial Impact:

- Higher credit card usage for non-essential purchases

- Reduced investment discipline

- Difficulty staying committed to long-term financial goals like an emergency fund or retirement corpus

4. Distorted Reality: What "Normal Spending" Looks Like

Spend enough time on social media and your benchmark for “normal” quietly shifts.

When you repeatedly see people posting about Rs 3,000 weekend brunches, Rs 50,000 gadgets, and international holidays every quarter, your brain begins to register those things as ordinary. This is called frequency bias, or the illusory truth effect. The more you see something, the more normal it begins to feel, regardless of whether it actually is.

Here is the reality: India’s gross domestic savings rate fell from 34.6% of GDP in 2011-12 to 29.7% in 2022-23, a near four-decade low, according to data from the Reserve Bank of India and ICRA. Yet consumption aspirations, driven heavily by social media and spending habits, continue to rise.

Financial Impact:

- Unrealistic lifestyle expectations

- A persistent feeling of financial inadequacy despite stable income

- Spending benchmarks that creep steadily upward year after year

5. FOMO Spending: Urgency That Costs You Money

“Only 3 left in stock!”

“Sale ends in 2 hours!”

“Thousands of people are already using this!”

These are not accidents. They are deliberate triggers rooted in what psychologist Robert Cialdini identified as the scarcity principle in his 1984 landmark book, Influence: The Psychology of Persuasion. When something feels scarce or time-limited, people assign it more value and act faster, often without thinking.

Social media and spending habits collide hardest at this exact point. Platforms surface these urgency triggers constantly in ads, in Stories, in countdown timers.

Financial Impact:

- Panic buying without proper research

- Poor purchasing decisions driven by artificial urgency

- Buyer’s remorse on items that felt urgent but were not needed

6. The Attention Economy: You're Not the Customer

Here is something worth sitting with.

You pay nothing to use Instagram, YouTube, or X. So how do these companies generate billions in revenue?

They sell access to your attention.

Every time you scroll, every video you watch, every link you click is a data point. That data is used to build a detailed profile of your behavior, interests, and vulnerabilities, which is then sold to advertisers who want to put the right product in front of you at the right moment.

Nobel Laureate Herbert A. Simon first articulated this concept in a 1971 paper titled “Designing Organizations for an Information-Rich World.” He wrote that a wealth of information creates a poverty of attention and that attention becomes the true scarce resource. Today, his insight forms the operating model of nearly every major social media platform on earth.

You are not the user. You are the product.

Financial Impact:

- Hyper-personalized ads that target your specific vulnerabilities

- A constant environment of spending triggers

- Exposure to temptation calibrated precisely to your psychological profile

7. The Real Damage: Small, Repeated Expenses

The danger is rarely one big, obvious purchase.

It is the Rs 499 impulse buy. The Rs 999 “limited deal.” The Rs 2,999 gadget you forgot you ordered by the time it arrived.

On their own, they feel insignificant. Added up, they are not.

Consider this: Rs 1,000 in social media-driven spending per week equals Rs 52,000 per year. If that same Rs 52,000 were invested annually in a mutual fund averaging 12% returns, after 10 years you would have approximately Rs 9 to 10 lakh verified using standard annuity calculations. That is the actual cost of treating small purchases as harmless.

This is not a hypothetical. This is compound interest working against you instead of for you.

How to Protect Your Money (Without Quitting Social Media)

Quitting social media is not realistic for most people, and it is not necessary. What matters is building intentional habits around how you engage with it.

1. Audit Your Feed

Unfollow accounts that consistently make you feel like you need to spend more. Follow financial educators, value-driven creators, and accounts that leave you feeling informed rather than inadequate. Your feed should work for your wealth, not against it.

2. Use the 24-Hour Rule

Before completing any unplanned online purchase, wait 24 hours. Most impulse buys triggered by social media and spending habits dissolve entirely when you give yourself time to think. This single habit alone can save thousands per year.

3. Create a “Scroll Budget”

Set a fixed monthly limit for discretionary, trend-based spending. When it is gone, it is gone. This one simple boundary makes impulse spending visible and controllable, which is the first step to stopping it.

4. Track Social Media-Driven Purchases

For one month, note every unplanned purchase and ask yourself two questions: Did I plan this? Did I see it on social media? Awareness alone is one of the most powerful tools for changing spending behavior around social media.

5. Shift from Consumption to Creation

Instead of passively scrolling, try creating. Write something. Build something. Share something. When you are in creator mode, you are far less susceptible to the passive influence that drives social media-related spending.

Final Thought: Your Feed Shapes Your Financial Future

Every post you engage with is quietly shaping what you want, what you believe you need, and how comfortable you feel spending money to get it.

Social media does not reach into your bank account directly. But it shapes the decisions that do.

The relationship between social media and spending habits is one of the most underestimated financial risks of our time. Platforms are only getting better at targeting you, and the gap between those who scroll with intention and those who scroll without it will show up in net worth over time.

Control your feed. Or it will control your finances.

FAQs

Does social media really affect spending habits?

Yes. It influences perception, desire, and decision-making, which directly impact spending.

Should I stop using social media?

Why do I feel poorer after scrolling?

Because of constant comparison and exposure to curated lifestyles.