How Lifestyle Inflation Destroys Financial Stability

Table of Contents

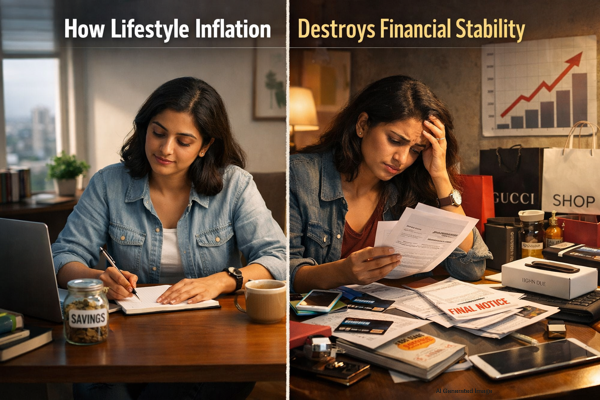

Discover how lifestyle inflation destroys financial stability. Lifestyle inflation silently drains your saving even as your income grows. Learn the warning signs, real money management tips.

You just got a salary hike. You treat yourself to a better phone, shift to a larger apartment, and start ordering from Swiggy four times a week instead of two. Life feels good.

But three months later, you check your savings account and wonder: where did all the money go?

This is lifestyle inflation doing its quiet, steady damage. It is one of the biggest threats to financial stability in India today, and most people do not even realize it is happening until it is too late.

Let us break it down clearly.

What is Lifestyle Inflation?

Lifestyle inflation, also called lifestyle creep, is the tendency to increase your spending every time your income goes up. It sounds harmless. After all, earning more and spending more feels natural. But here is the problem: when your expenses always rise to meet your income, your savings never grow.

It rarely hits you all at once. Lifestyle creep happens gradually:

- You switch from a budget smartphone to a flagship model

- You add a few premium OTT subscriptions

- You start eating out more frequently

- You opt for a bigger flat with a higher rent

Each of these feels like a reasonable upgrade. But together, they silently eat into your ability to build long-term wealth.

Why Lifestyle Inflation is Dangerous

1. You May Earn More but Still Not Build Wealth

This is the harsh truth that most high earners discover eventually. A person earning Rs. 1.5 lakh per month but spending Rs. 1.45 lakh is in a far worse financial position than someone earning Rs. 60,000 and saving Rs. 15,000 consistently.

According to personal finance research, your savings rate matters far more than your income level when it comes to building long-term wealth. Lifestyle inflation keeps your savings rate close to zero, no matter how many raises you receive.

2. Savings and Investments Get Reduced

When lifestyle inflation takes hold, saving becomes an afterthought. You spend first and save whatever is left, which is often nothing.

This directly hurts your financial stability in three critical areas: your emergency fund dries up or never gets built, retirement planning gets pushed to “next year,” and your investments shrink or stagnate entirely.

Fewer investments mean you miss out on the power of compounding. According to financial planning guidelines widely used in India, money invested in a diversified mutual fund over 15 to 20 years can grow exponentially compared to money invested for just 5 to 10 years.

3. It Creates Dependency on a High Income

Once you build a lifestyle around a certain income, it becomes very hard to scale back. Your fixed monthly expenses go up, whether that is rent, EMIs, or club memberships.

This dependency reduces your career flexibility. You cannot afford to take a career break, explore entrepreneurship, or switch to a more fulfilling but lower-paying job. Financial stress becomes a constant companion, especially during periods of job loss or economic slowdown.

4. It Increases Financial Stress

Here is the irony of lifestyle inflation: it often makes people feel more financially stressed, not less. Higher spending leads to higher fixed commitments every single month. EMIs pile up. Credit card bills swell. Even someone earning Rs. 2 lakh per month can feel financially suffocated if lifestyle creep has taken over.

This is a well-documented financial psychology pattern. Spending on lifestyle upgrades delivers a short burst of satisfaction but rarely improves long-term happiness in a meaningful way.

5. It Delays Wealth Creation

The longer you delay investing, the more you lose to the compounding gap. A simple example: if you invest Rs. 10,000 per month starting at age 25, you accumulate far more by age 60 than someone who starts at 35 with Rs. 20,000 per month, even though the second person invests more money in absolute terms.

Lifestyle inflation is the single biggest reason people delay the start of their investment journey in personal finance India. Every rupee spent upgrading your lifestyle today is a rupee that does not compound for your future.

A Simple Example

Consider two professionals working in the same city:

Person A earns Rs. 50,000 per month and saves Rs. 10,000 every month without fail.

Person B earns Rs. 1,00,000 per month but spends it all on a premium lifestyle with zero savings.

After 10 years, assuming Person A invests in a mutual fund SIP averaging 12% annual returns, their corpus grows to approximately Rs. 23 lakh. Person B has nothing, despite earning twice as much.

The math is clear. Financial stability is built through consistent savings, not a high salary.

Signs You're Experiencing Lifestyle Inflation

Watch out for these red flags in your own spending patterns:

- Your monthly expenses jump after every salary hike

- You earn well but struggle to save consistently

- You rely on credit cards or personal loans to manage month-end expenses

- You keep upgrading gadgets, clothing, or vehicles without planning

- Despite multiple promotions, your net worth has barely moved

If two or more of these sound familiar, lifestyle creep may already be at work.

How to Avoid Lifestyle Inflation

1. Follow the “Save First, Spend Later” Rule

This is the foundational rule of smart money management. Before you pay for anything else, set aside your savings. Most financial advisors in India recommend a savings rate of at least 20% of take-home income. As your income grows, push that number toward 30% to 40%.

The moment you reverse the habit from “save what is left” to “spend what is left after saving,” your financial trajectory changes completely.

2. Increase Savings When Income Increases

Every time you receive a salary hike or bonus, make a rule for yourself: save at least 30% to 40% of the increment before you think about lifestyle adjustments.

This one habit alone can dramatically accelerate your journey toward financial stability. Your lifestyle can improve, but your savings must improve faster.

3. Delay Lifestyle Upgrades

You got a raise in April. Give yourself until October before making any major lifestyle change. Those 6 months allow you to build your emergency fund, top up your SIPs, and think clearly about whether the upgrade is genuinely worthwhile.

Impulse lifestyle upgrades are the most common driver of lifestyle inflation. A waiting period helps you filter needs from wants.

4. Automate Your Investments

One of the most effective money management tips is to remove the human decision from investing. Set up automatic SIPs in mutual funds, contribute to your PPF account monthly, and automate your NPS contributions if applicable.

When the money moves out of your account before you can spend it, lifestyle inflation has no fuel to grow.

5. Understand the Difference Between Needs and Wants

This sounds simple but requires consistent practice. Before any non-essential purchase, ask yourself: will this meaningfully improve my quality of life three months from now, or does it just feel exciting today?

Most lifestyle upgrades fail that test.

6. Use EMIs Wisely

EMIs are not inherently bad. A home loan EMI is building a long-term asset. But an EMI on a new phone, a luxury watch, or a furniture upgrade is a different story altogether.

As a general rule, avoid lifestyle inflation through EMIs. If you cannot pay for a lifestyle upgrade in cash without disturbing your savings, you likely cannot afford it yet.

7. Set Clear Financial Goals

People who have defined financial goals resist lifestyle inflation more effectively. When you know you want to buy a home in five years or retire at 55, every spending decision runs through that filter first.

Write down your goals. Assign a rupee value and a timeline to each one. This turns your money from something you spend into something that works for you.

A Simple Rule to Follow

Think of it this way:

Income goes up. Savings go up faster. Lifestyle upgrades happen last and within limits.

That one shift in priority is the difference between people who build real wealth and people who wonder at 50 why their income was always high but their savings never were.

Conclusion

Lifestyle inflation does not feel like a problem when it is happening. Every upgrade makes sense in the moment. But the cumulative damage it does to your savings, your investments, and ultimately your financial freedom is very real.

The goal here is not to live like a minimalist or refuse yourself any pleasure. Enjoy the fruits of your hard work. But do it with intention, not just by default.

Because genuine financial stability in India, or anywhere else, has never been about how much money comes in. It is always about how much you keep, grow, and protect over time.

Control your lifestyle before your lifestyle controls your finances.

FAQs

Is lifestyle inflation always bad?

No. Improving your lifestyle is natural, but it should be gradual and aligned with your financial goals.

How much should I ideally save?

Start with at least 20% of your income, and aim to increase it as your earnings grow.

Can high earners also face this problem?

Yes. In fact, higher income often leads to higher spending, making lifestyle inflation more common among high earners.

What’s the easiest way to control lifestyle inflation?

Disclaimer

This article is for educational purposes only and should not be considered financial advice. Please consult a qualified financial advisor before making financial decisions.