Why High Income Doesn't Guarantee Wealth | Habits That Build Real Financial Freedom

Table of Contents

Earning a high income is a great start , but it is not enough. Discover why high income doesn’t guarantee wealth creation and the financial habits that actually build long-term financial freedom.

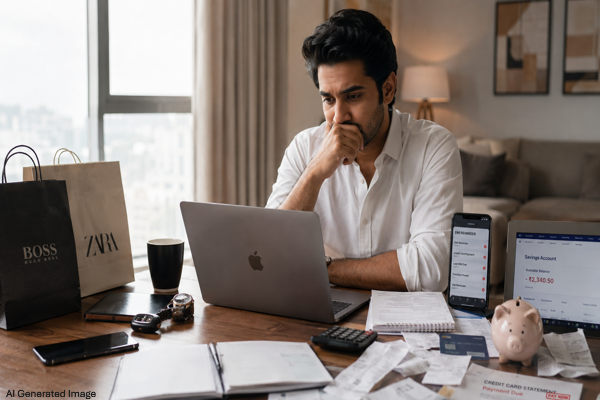

Think about the last time you heard about a doctor buried in debt or a corporate executive living paycheck to paycheck. Surprising, right? These are people earning lakhs every month, sometimes more than most people see in a decade. And yet, financial stress follows them around like a shadow.

On the flip side, you probably know someone with a modest salary who owns their home outright, holds solid investments, and sleeps well without worrying about money. How does that happen?

The answer is simple: a high income and actual wealth are two completely different things.

Income vs Wealth: Understanding the Difference

Income is the money flowing into your life regularly. That includes salary, freelance work, business profits, rental earnings, and investment returns. Think of it like water running out of a tap.

Wealth, on the other hand, is what you actually have left over. It is the total value of your assets after subtracting your liabilities. Think of it as water stored in a tank, not the water flowing through the pipe.

You can have a powerful tap and still have an empty tank if the water keeps draining out faster than it fills up.

A practical way to frame it: Wealth = What You Keep, Not Just What You Earn.

A person earning Rs 30 lakh a year but spending Rs 28 lakh of it is not building wealth. They are building appearances. Meanwhile, someone earning Rs 9 lakh a year and consistently investing Rs 2 lakh of it is quietly compounding their way toward real financial security.

The Biggest Financial Myth About High Income

Here is one of the most stubborn beliefs in personal finance: “Once I start earning more, all my money problems will disappear.”

The data tells a different story. According to a LendingClub and PYMNTS report published in January 2023, 51% of consumers earning over $100,000 annually were living paycheck to paycheck as of December 2022. Higher income did not automatically solve financial stress. It just made the lifestyle more expensive.

As income rises, spending habits almost always follow. New salary, new car. Promotion, bigger apartment. Bonus, overseas vacation. Without financial discipline, a higher salary simply creates a bigger lifestyle, not greater wealth creation.

Lifestyle Inflation: The Hidden Trap

Lifestyle inflation is one of the biggest silent threats to long-term wealth building. It is the gradual habit of spending more as you earn more, turning yesterday’s luxuries into today’s bare minimums.

You get a salary hike and buy a better phone. A year later, that phone feels ordinary and you want another upgrade. You move into a larger home with a heavier EMI. You start flying business class, dining at premium restaurants, and collecting premium memberships.

None of these choices are wrong on their own. The problem starts when every additional rupee of income gets absorbed into higher fixed monthly costs before you have set aside anything for investing.

The result is predictable: high income, high expenses, low net worth.

Why Some High Earners Still Struggle Financially

Spending to Impress Others

Social pressure is real and expensive. Many high-income individuals spend heavily on luxury brands, lavish weddings, and visible status symbols. The goal, consciously or not, is to look wealthy rather than to actually become wealthy.

Research published in the Journal of Consumer Research suggests that genuinely wealthy individuals often live far more conservatively than people expect. The loudest spender in the room is usually the one with the smallest net worth.

Depending Only on Salary

A single income source, no matter how large, is fragile. Job loss, burnout, industry disruption, or a health crisis can shut it down overnight.

Real wealth builders develop multiple income streams over time, including equity investments, dividend income, rental properties, or side businesses. This is not about grinding around the clock. It is about building financial resilience so that your financial life does not collapse if your job does.

Ignoring Investments

High earners tend to be busy people, and that busyness becomes a ready excuse to delay investing.

“I will sort it out later.”

“I already earn well, so I am fine.”

“I do not have time to research the options.”

But wealth creation through investing is not just about picking the right stocks. It is about time in the market. The earlier you start, the more compounding works in your favor, and the less heavy lifting your income has to do.

The Power of Compounding

Compounding is arguably the most powerful force in personal finance. The math is simple but the results are remarkable.

If you invest Rs 10,000 per month starting at age 25, at a 12% annual return consistent with long-term Indian equity market averages, you could accumulate over Rs 3.5 crore by age 55. Start the same monthly investment at age 35 and that figure drops to roughly Rs 1 crore.

The difference is not in the amount invested. The difference is time. Consistent investing, even in moderate amounts, outperforms large irregular investments over the long run every single time.

Taking Excessive Debt

High income comes with high loan eligibility. Banks are happy to approve large home loans, car loans, and generous credit card limits for strong earners.

But loan eligibility is not the same as affordability. Large EMIs reduce monthly cash flow, limit your ability to invest, and create financial pressure that compounds over years. A high-income individual carrying Rs 3 lakh in monthly EMIs has far less wealth-building capacity than someone with lower income and near-zero debt.

Lack of Financial Planning

Perhaps the most surprising pattern: many high-income professionals have no real financial plan. No emergency fund target, no retirement number in mind, no investment schedule, no clear budget.

Earning well without a financial plan is like running a business without bookkeeping. The money comes in, the money goes out, and at the year-end you cannot quite figure out where it all went.

Real Wealth Is Usually Built Quietly

Social media has created a distorted picture of what wealthy people look like. The reality is far less exciting to photograph.

Long-term wealth creation looks like skipping an impulsive weekend purchase, sticking to a SIP that has been running for nine years, and choosing a practical car over a status symbol. It is slow, disciplined, and thoroughly unglamorous.

The people who reach genuine financial freedom are rarely the highest earners in the room. They are almost always the most financially disciplined.

Signs You Are Earning Well but Not Building Wealth

Watch for these patterns in your own financial life:

Your expenses climb after every salary increase. You save very little despite a strong income. You depend entirely on next month’s paycheck to meet current obligations. Your credit card balance rolls over month after month. Your investments are sporadic at best. Most of your purchases are driven by what others will think, not by what you actually need.

If any of these feel familiar, the issue is probably not your income. The issue is your financial behavior.

How to Turn High Income Into Real Wealth

Raise your savings rate, not just your lifestyle. Each time your income increases, direct a meaningful portion toward investments before adjusting your lifestyle upward.

Automate your investing. Set up a monthly SIP, schedule automatic transfers to your investment accounts, and remove the decision from your hands entirely. Automation kills the temptation to skip months.

Manage lifestyle inflation deliberately. Enjoy what you earn. Just avoid turning every want into a permanent monthly financial commitment.

Build assets, not just income. Equity mutual funds, direct stocks, productive real estate, and even valuable skills generate future value. EMIs on depreciating assets quietly work against you.

Avoid debt that does not create value. A home loan on an appreciating property is fundamentally different from a personal loan for a vacation. Knowing the difference protects your wealth.

Think in decades, not months. Patience is one of the most underrated financial skills. The 30-year investor consistently outperforms the 3-year speculator.

Rich vs Wealthy: There Is a Big Difference

Being rich typically means high spending, a visible lifestyle, and financial pressure tied entirely to active income. Being wealthy means holding strong investments, maintaining financial security, generating passive income, and having freedom from money anxiety.

The goal should not simply be to earn more. The real goal is financial freedom and peace of mind.

Final Thoughts

A high income is a powerful tool. But tools only work when used correctly.

Without disciplined spending, consistent investing, and a long-term financial plan, even a very large salary can quietly evaporate over the years. Real wealth is built through consistent investing, smart financial habits, controlled lifestyle choices, and a great deal of patience.

At the end of the day, wealth is less about how much you earn and more about how wisely you manage what you earn.

FAQs

Can someone with an average income become wealthy?

Yes. Consistent saving, disciplined investing, and avoiding unnecessary debt can help average earners build wealth over time.

Why do some high earners live paycheck to paycheck?

Is a salary enough to become wealthy?

A salary can absolutely help build wealth, especially when combined with disciplined saving and investing.

What is the biggest mistake high earners make?

Does wealth mean owning expensive things?

No. Wealth is about financial security, assets, and long-term freedom not appearances.

Disclaimer

This article is for educational purposes only and should not be considered financial or investment advice. Please consult a qualified financial advisor before making financial decisions.