How Salaried Employees Can Build Long-Term Wealth

Discover how salaried employees can build long-term wealth with SIPs, tax-saving investments, emergency funds, and smart financial strategies. Start your wealth-building journey today.

Let’s be honest a salary hitting your bank account every month feels great, but it does not automatically make you wealthy. Most salaried professionals in India spend years chasing increments and promotions without ever truly building financial security. The truth is, building long-term wealth as a salaried employee in India is less about how much you earn and more about what you do with what you earn.

From Mumbai to Bengaluru, from a ₹30,000 monthly take-home to a ₹1.5 lakh package the principles of wealth creation remain the same. Disciplined saving, consistent investing, and a clear financial plan are the real foundations. In this blog, we will walk through practical, no-jargon strategies that any Indian salaried professional can follow to build long-term wealth in a realistic and sustainable way.

1. Start With a Clear Financial Plan

Before you invest a single rupee, ask yourself what am I actually investing for? It sounds like an obvious question, but most salaried employees skip this step entirely. They invest because a colleague mentioned a stock, or because their insurance agent called, or simply because tax season arrived. That is not a financial plan that is financial chaos.

A proper financial plan for salaried individuals covers:

- Buying a house in the next 8–10 years

- Children’s education expenses 15 years down the line

- A comfortable retirement corpus by age 55 or 60

- Achieving financial independence the freedom to work by choice, not compulsion

When your goals are clear, every financial decision becomes easier. You will know how much to invest, which products make sense for your situation, and most importantly you will stay the course during market ups and downs instead of panicking.

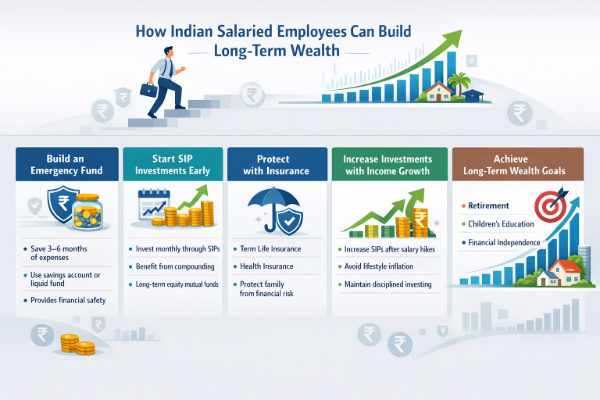

2. Build an Emergency Fund First

Here is a mistake many salaried professionals make they jump straight into investing without any financial cushion. Then one day, the car breaks down or a family member needs hospitalization, and suddenly they are forced to break their investments at the worst possible time.

An emergency fund is not glamorous, but it is absolutely non-negotiable before you start long-term wealth creation. Financial planners consistently recommend building a reserve of at least 6 to 12 months of living expenses. Keep this money in safe, easily accessible options such as a high-interest savings account, liquid mutual funds, or short-term fixed deposits.

Think of it this way your emergency fund is the reason your long-term investments get to stay long-term.

3. Start Investing Early to Benefit From Compounding

Warren Buffett did not become one of the world’s richest investors simply by picking the right stocks. He made his very first stock purchase at just 11 years old and let compounding do the heavy lifting for decades. The same principle works just as powerfully for a salaried employee in India.

Compounding means that your returns start generating their own returns over time. A monthly SIP of ₹10,000 started at age 25 can grow to approximately ₹1.8–1.9 crore over 25 years, assuming average annual returns of around 12%. Of course, market returns are never guaranteed and will vary but the point is simple: time is your most powerful wealth-creation asset, and you cannot buy it back once it is lost.

If you are in your 20s or early 30s right now, you have something more valuable than a big salary you have time. Use it.

4. Use SIPs for Consistent Investing

A Systematic Investment Plan, or SIP, is perhaps the most salaried-employee-friendly investment tool available in India today. The idea is simple you invest a fixed amount every month into a mutual fund, just like an EMI, except this one is building your future rather than paying for your past.

SIPs work brilliantly for several reasons. They remove the temptation to time the market a game that even professional fund managers rarely win consistently. When markets fall, your SIP buys more units at lower prices. When markets rise, the value of those units grows. Over time, this averaging effect smooths out the inevitable volatility of equity markets.

Start with whatever amount is affordable even ₹500 or ₹1,000 a month and scale it up as your income grows. The discipline of an automated monthly investment is more important than the amount, especially in the early years.

5. Invest in Equity for Long-Term Growth

Many Indian salaried professionals still keep the bulk of their savings in fixed deposits and savings accounts. While these are safe, they often struggle to beat inflation over long periods meaning your money is technically growing but actually losing purchasing power.

Historically, Indian equity markets have delivered significantly higher long-term returns compared to most traditional investment options, though short-term volatility is unavoidable. For salaried investors, the most practical ways to gain equity exposure include equity mutual funds, index funds that track benchmarks like the Nifty 50, or direct stocks for those with experience and interest.

If you are just starting out, diversified mutual funds or Nifty index funds are an excellent choice low cost, broadly diversified, and managed without requiring you to track individual companies.

6. Use Tax-Saving Investments Wisely

Tax planning is not just an annual ritual to be handled in March it is an integral part of smart financial planning for any salaried employee in India. Under Section 80C of the Income Tax Act, you can claim deductions of up to ₹1.5 lakh per year by investing in specific instruments.

Important: These deductions are available only under the old tax regime. Since the Finance Act 2023, the new tax regime is the default for all salaried individuals. If you have not actively opted for the old tax regime with your employer, you are already in the new regime and cannot claim 80C benefits. Make sure you consciously choose the old tax regime during your investment declaration if you intend to use these tax-saving instruments.

Some of the most effective tax-saving investments available include:

- Public Provident Fund (PPF) — safe, tax-free returns over 15 years

- Equity Linked Savings Scheme (ELSS) — tax-saving mutual funds with a 3-year lock-in and equity growth potential; note that long-term capital gains above ₹1.25 lakh are taxed at 12.5% (updated as of Budget 2024)

- Employees’ Provident Fund (EPF) your employer-linked retirement savings that build quietly every month

The key is to choose tax-saving investments that align with your broader financial goals not just those that promise the highest deduction on paper.

7. Increase Investments When Your Salary Increases

You got that appraisal. Great. Now comes the real test do you upgrade your lifestyle, or do you upgrade your wealth-building journey? Most people fall into the first category without even realizing it.

A simple and powerful strategy is the step-up SIP approach. Every year, when your salary increases, increase your SIP amount by 10–15% as well. If you receive a bonus, deploy at least a portion of it into investments rather than spending all of it.

The math here is compelling. A SIP that starts at ₹10,000 and steps up by just 10% annually will accumulate significantly more wealth over 20 years than one that remains flat. Your income trajectory is an asset make it work for your financial goals.

8. Avoid Lifestyle Inflation

Lifestyle inflation is the silent killer of wealth creation. It is the tendency to spend more as you earn more a newer phone every year, a bigger car after the next promotion, dining out more often, premium streaming subscriptions, frequent holidays. None of these things are wrong in themselves, but when they all expand together to consume every rupee of a salary hike, long-term wealth creation stalls.

A practical and sustainable approach is to target saving and investing at least 20–30% of your monthly income. As your income grows, try to keep this percentage intact or better, increase it. You can absolutely enjoy life and spend on things that matter to you, but do it consciously rather than by default.

Wealth is not built by people who earn the most. It is built by people who spend mindfully and invest consistently.

9. Review Your Investments Periodically

Investing is not a one-time task you set up and never look at again but it is also not something you need to obsess over daily. The right balance is a periodic review once or twice a year to make sure everything is on track.

During your annual portfolio review, check whether:

- Your investments still align with your financial goals

- Your asset allocation between equity and debt remains balanced for your risk profile

- Any underperforming funds need to be replaced or reconsidered

Avoid the trap of checking your portfolio every day or every week. Short-term market movements are noise. Reacting emotionally to every dip or rally is one of the most common ways investors destroy long-term wealth.

10. Plan Early for Retirement

Retirement feels impossibly far away when you are 25 or 30. That is exactly why most people put off planning for it and end up scrambling in their 50s. The irony is that the earlier you start, the less you actually need to invest each month to build a meaningful retirement corpus.

Useful options for retirement planning in India include:

- National Pension System (NPS) — market-linked returns with additional tax benefits under Section 80CCD(1B), offering an extra ₹50,000 deduction over and above the 80C limit (available under the old tax regime)

- Employees’ Provident Fund (EPF) a consistent foundation for every salaried professional

- Long-term SIPs in equity mutual funds the most flexible way to build a retirement corpus over decades

Starting even five years earlier can make a dramatic difference in your final retirement fund. Time and compounding together are a combination that simply cannot be replicated with a larger investment made later.

Key Takeaways

Building long-term wealth as a salaried employee in India does not require a finance degree, a massive salary, or access to complicated investment products. It requires something far more ordinary discipline, patience, and the willingness to start.

To summarise the habits that matter most:

- Start investing as early as possible time is your greatest financial asset

- Build a solid emergency fund before chasing long-term growth

- Invest consistently every month through SIPs automate it so it happens without willpower

- Increase your investment amount every time your income grows

- Plan for taxes proactively using 80C and other available deductions but only if you are on the old tax regime

- Guard against lifestyle inflation it is the most common wealth leak for salaried professionals

- Review your portfolio annually and stay the course through short-term volatility

- Start retirement planning early your future self will thank you

None of this is rocket science. But executed consistently over 15–25 years, these simple habits have the power to transform an ordinary salary into extraordinary wealth. The best time to start was yesterday. The second-best time is today

FAQs

How much should a salaried employee invest every month?

Are mutual funds suitable for salaried investors?

Yes. Mutual funds, especially through SIPs, allow investors to invest small amounts regularly, making them suitable for salaried individuals.